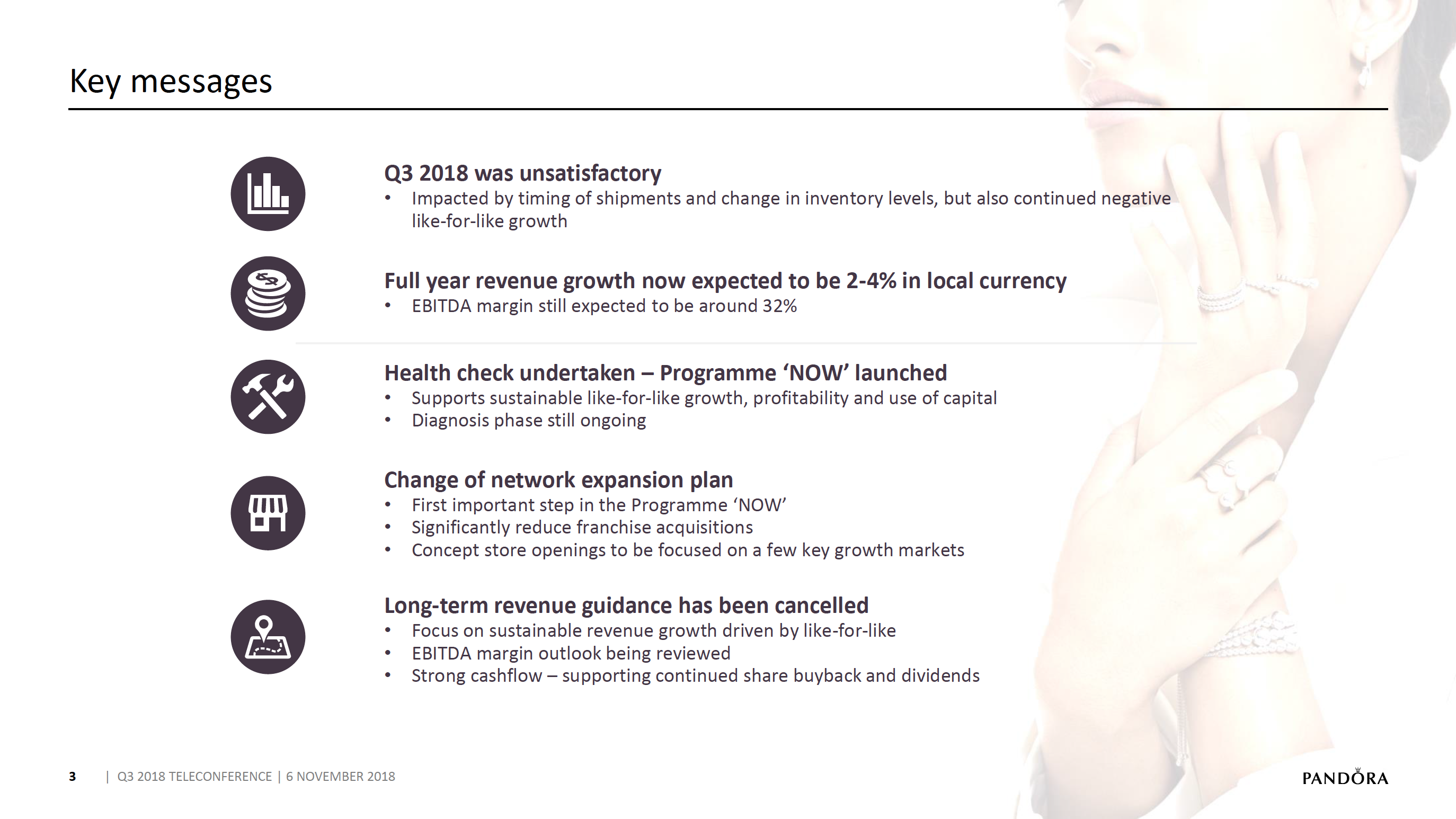

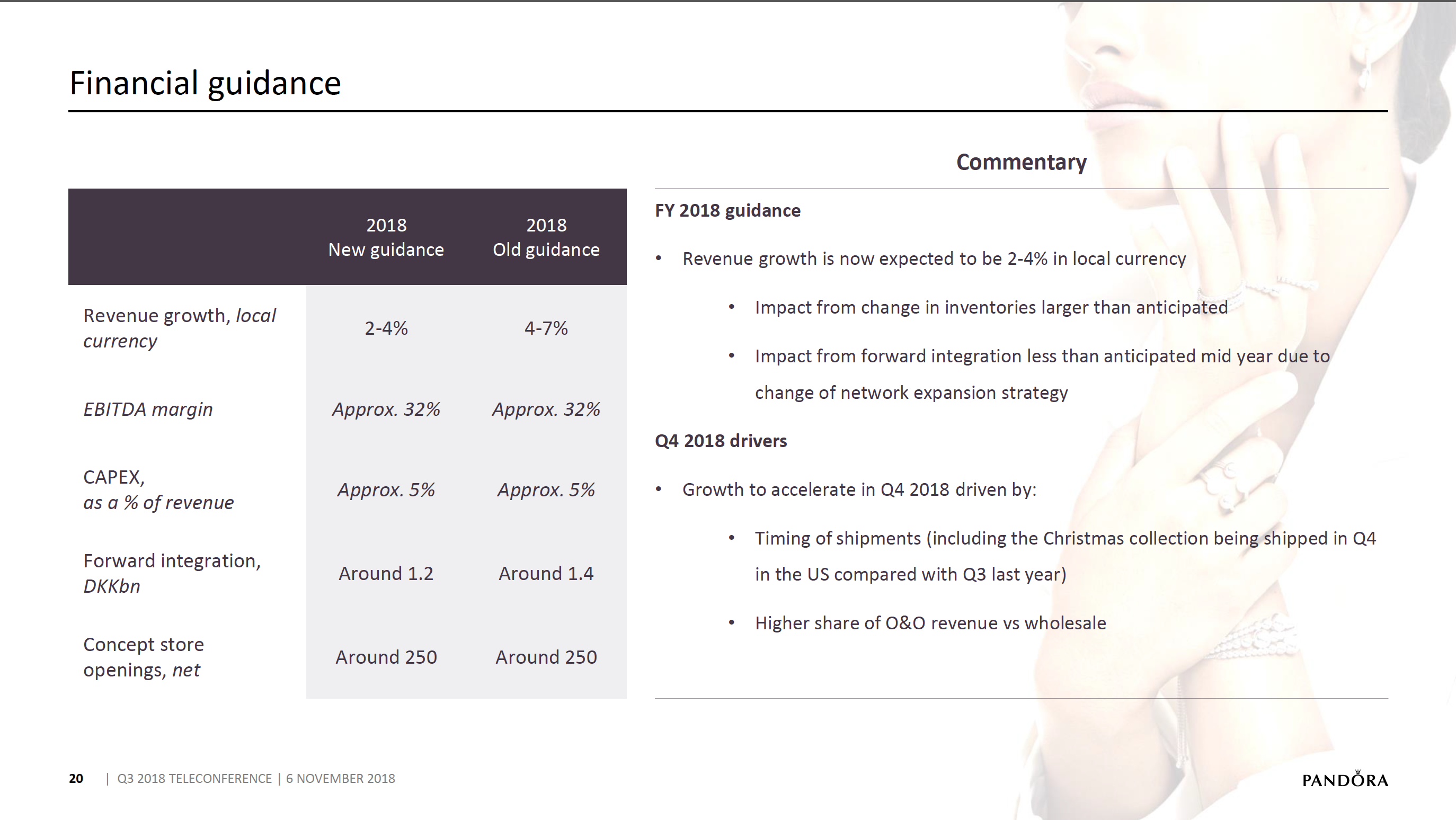

The jewelry maker Pandora, which is still without a CEO, sent out a press release on their Q3 results today. Expected revenue growth for 2018 was revised from 4-7% to 2-4%.

Bloomberg: Pandora Plans `Reset’ in Bid to Shore Up Investor Confidence

Reuters: Charm-bracelet maker Pandora warns again on sales

euronews: Jeweller Pandora cuts 2018 sales outlook, reviews long-term profit target

Financial Times: Pandora cuts growth forecast as profits and sales miss in third quarter

Børsen: Derfor vendte Pandora-aktien rundt fra et to-cifret kurshug til et lille fald

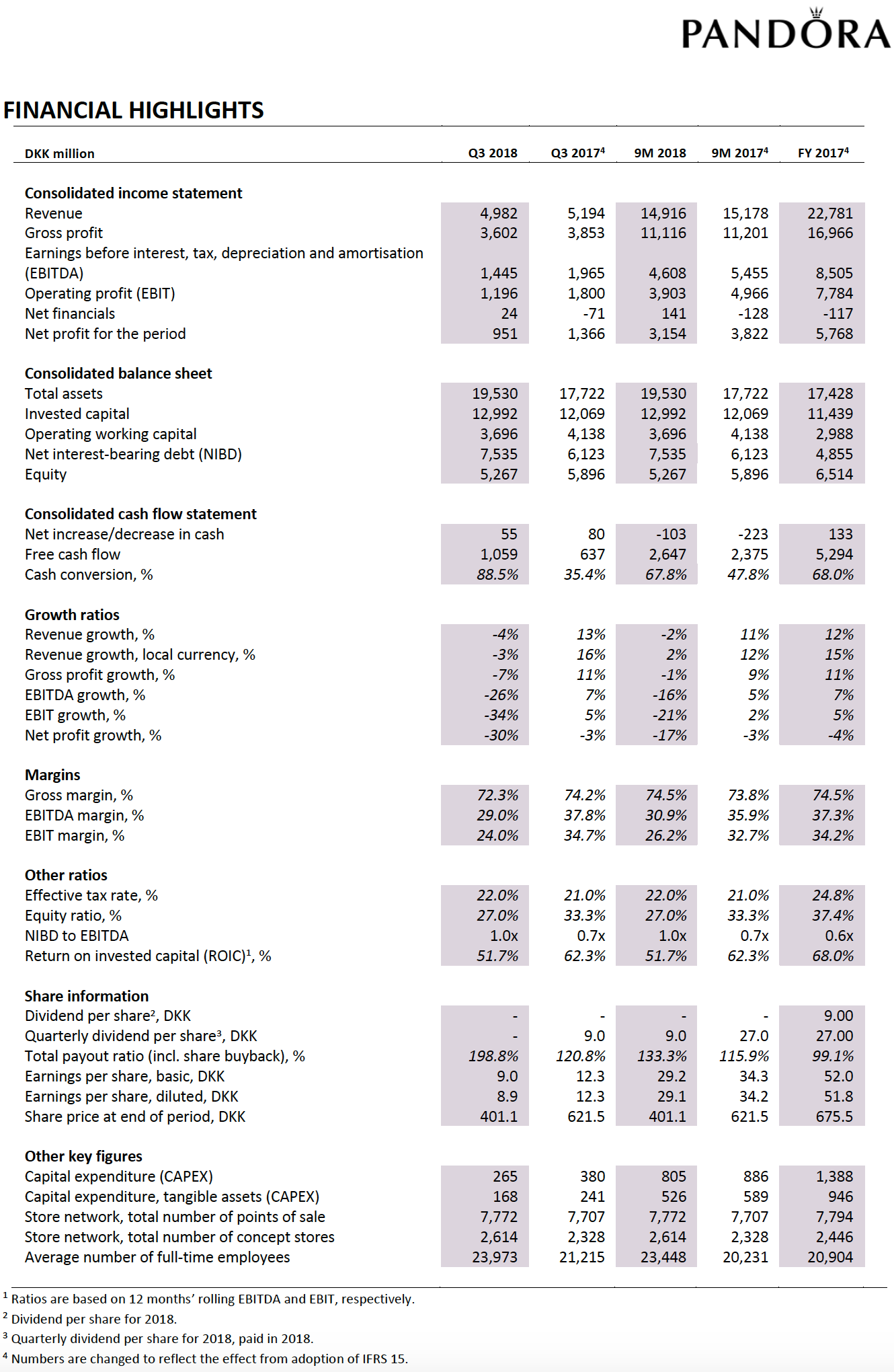

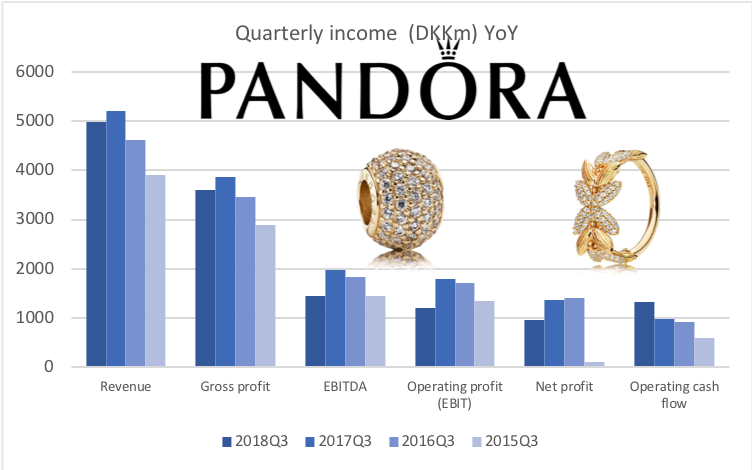

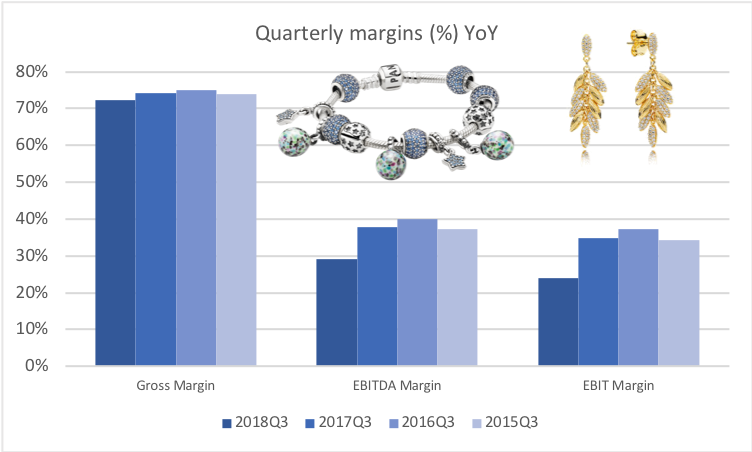

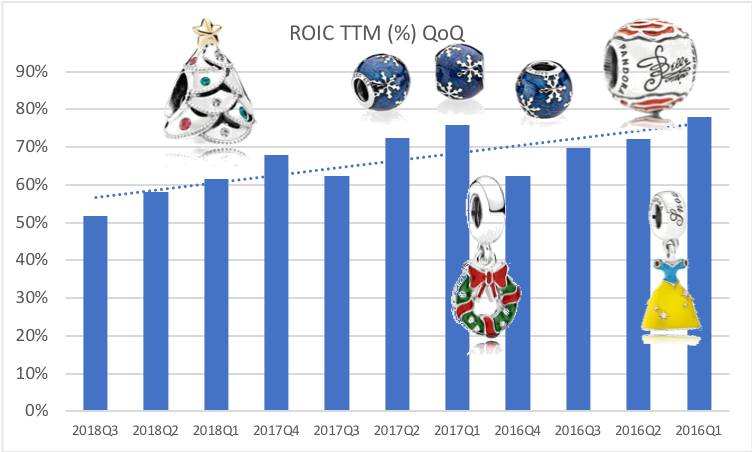

Below are 4 slides from the earnings call and and 1 page from the earnings release summarising the key metrics, financial highlights and revised outlook.

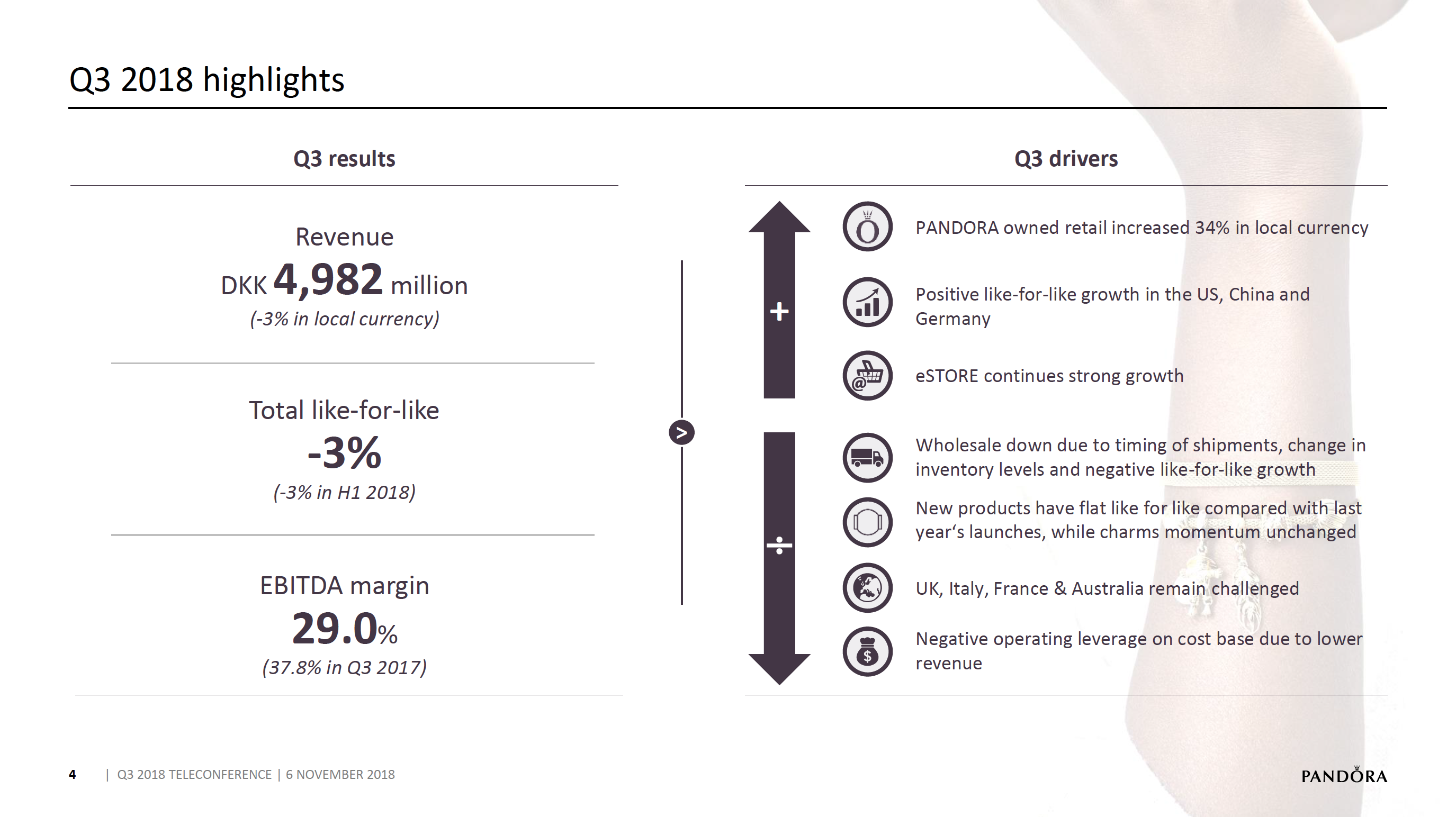

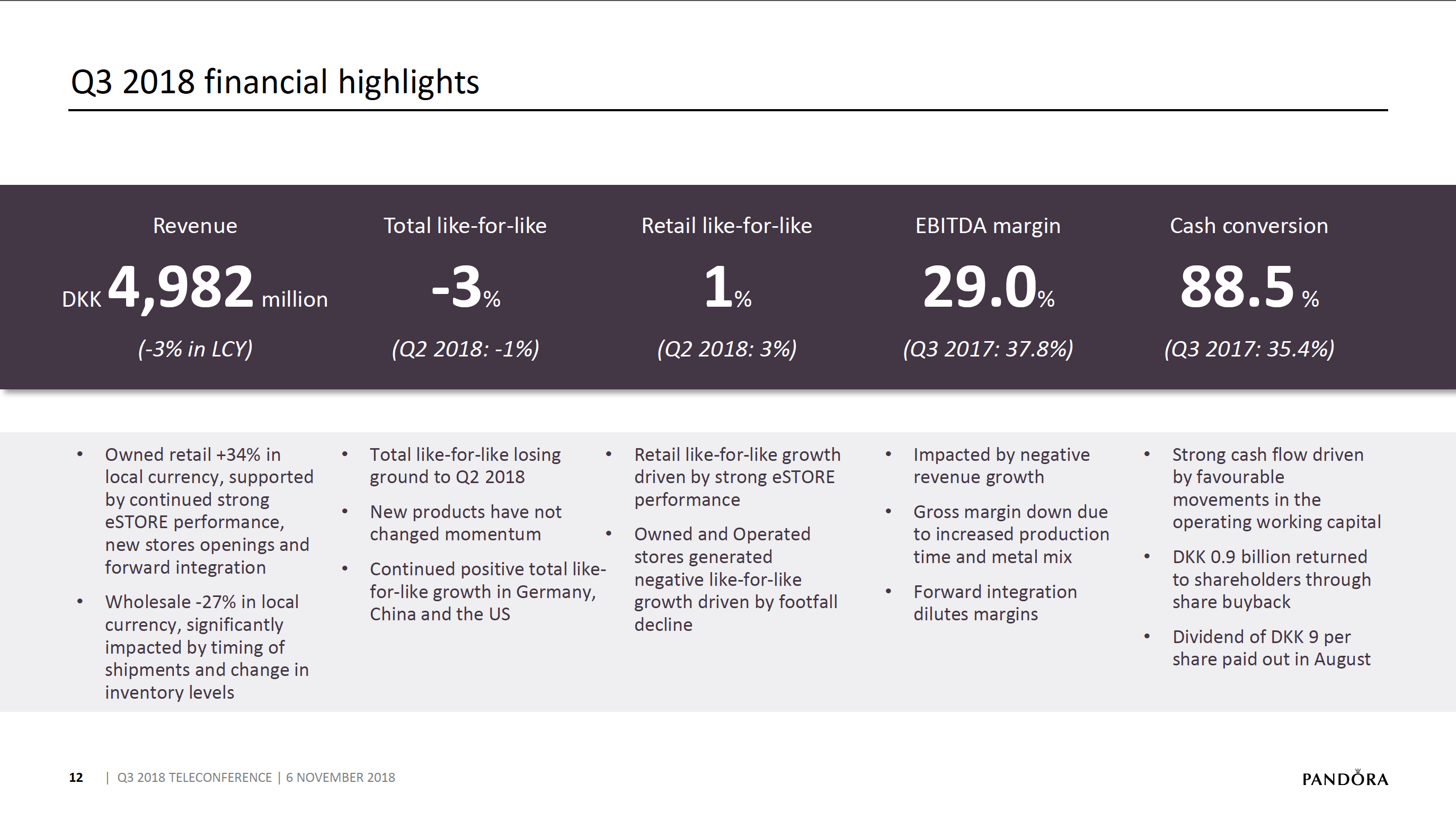

Revenue was down YoY by 3% in local currency and all margins were down as well. Operating cash flow was up due to fluctuations in operating working capital.

The ROIC dropped to an all time low of 51.7%.

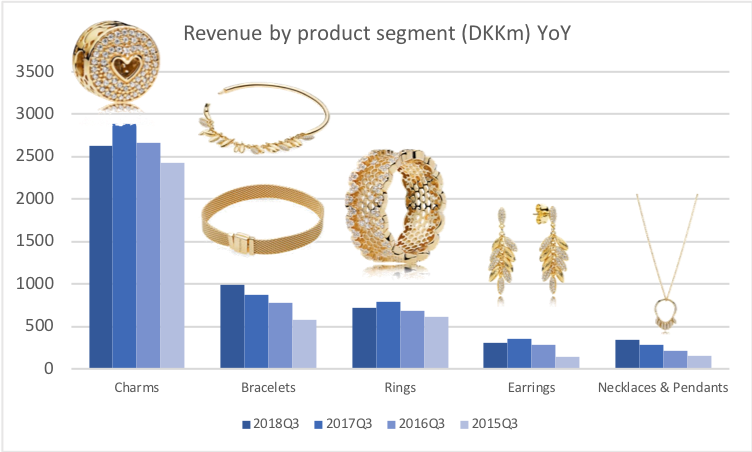

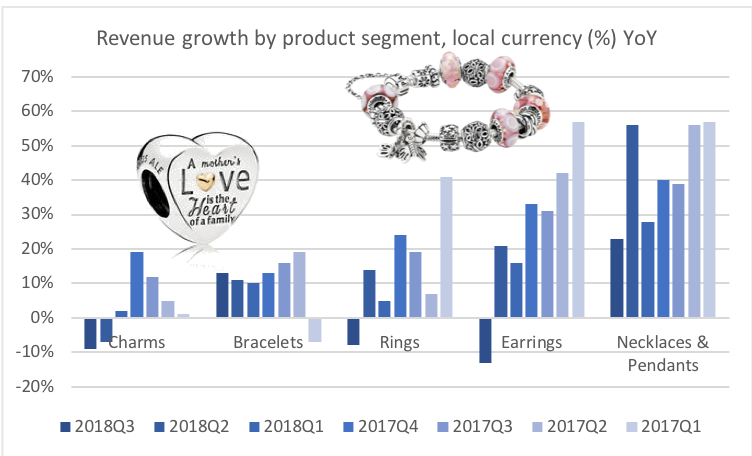

Revenue from charms was down YoY along with rings and earrings.

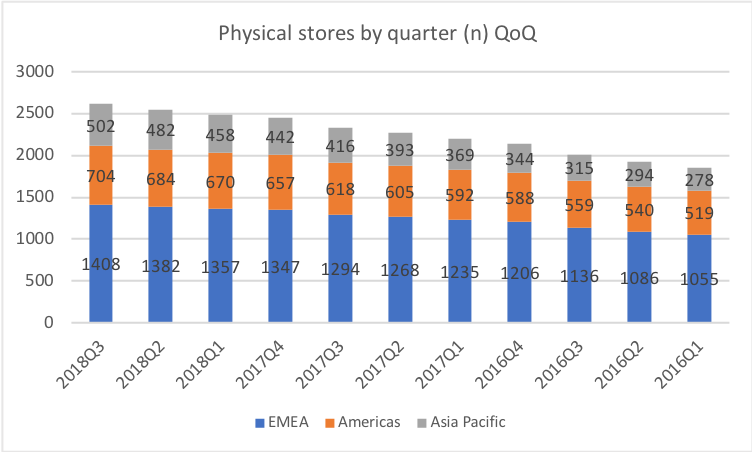

The number of stores was up QoQ and YoY, but the strategy of aggressive store expansion might come to an end in 2019, and the focus will be switched to same store sales growth. The diagnosis is ongoing.

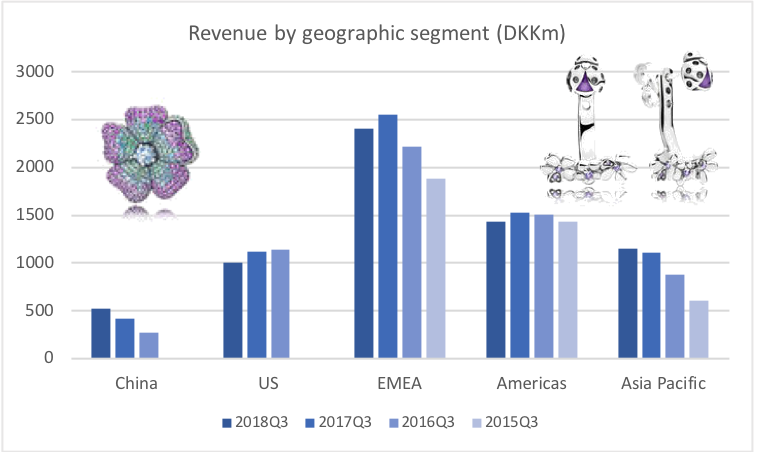

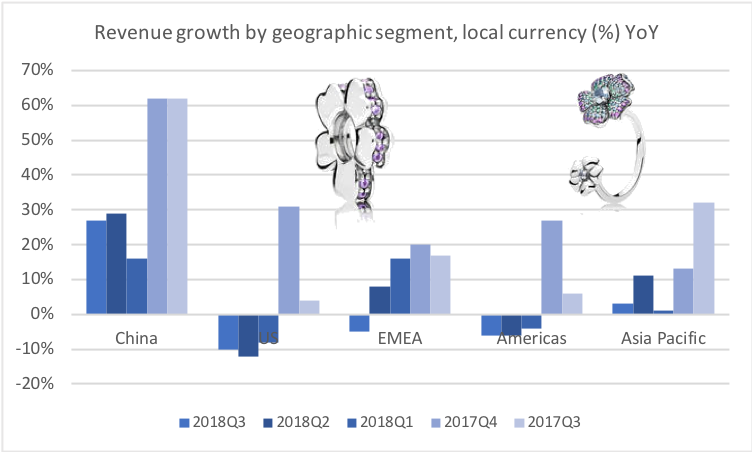

Revenue in China was up and held revenue in APAC up, which would otherwise have been down like EMEA and Americas.

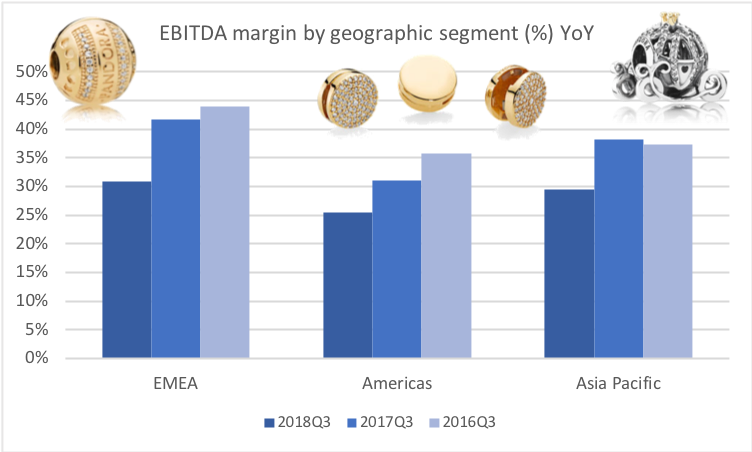

Likewise the EBITDA margin was down in all three regions.

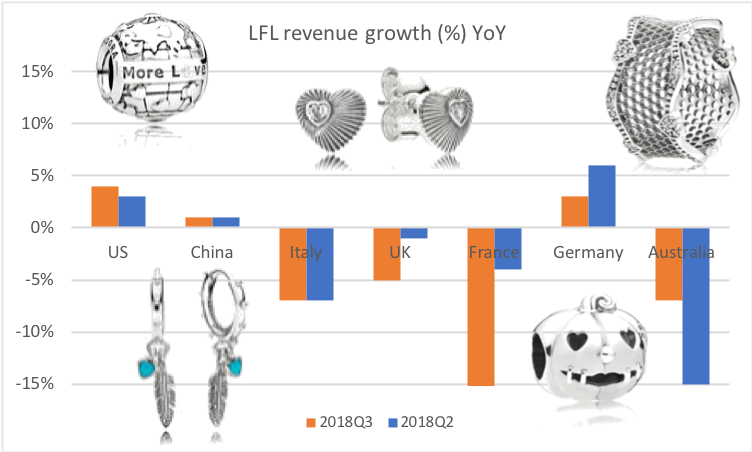

Only three of the seven largest markets experienced positive growth in same store sales.

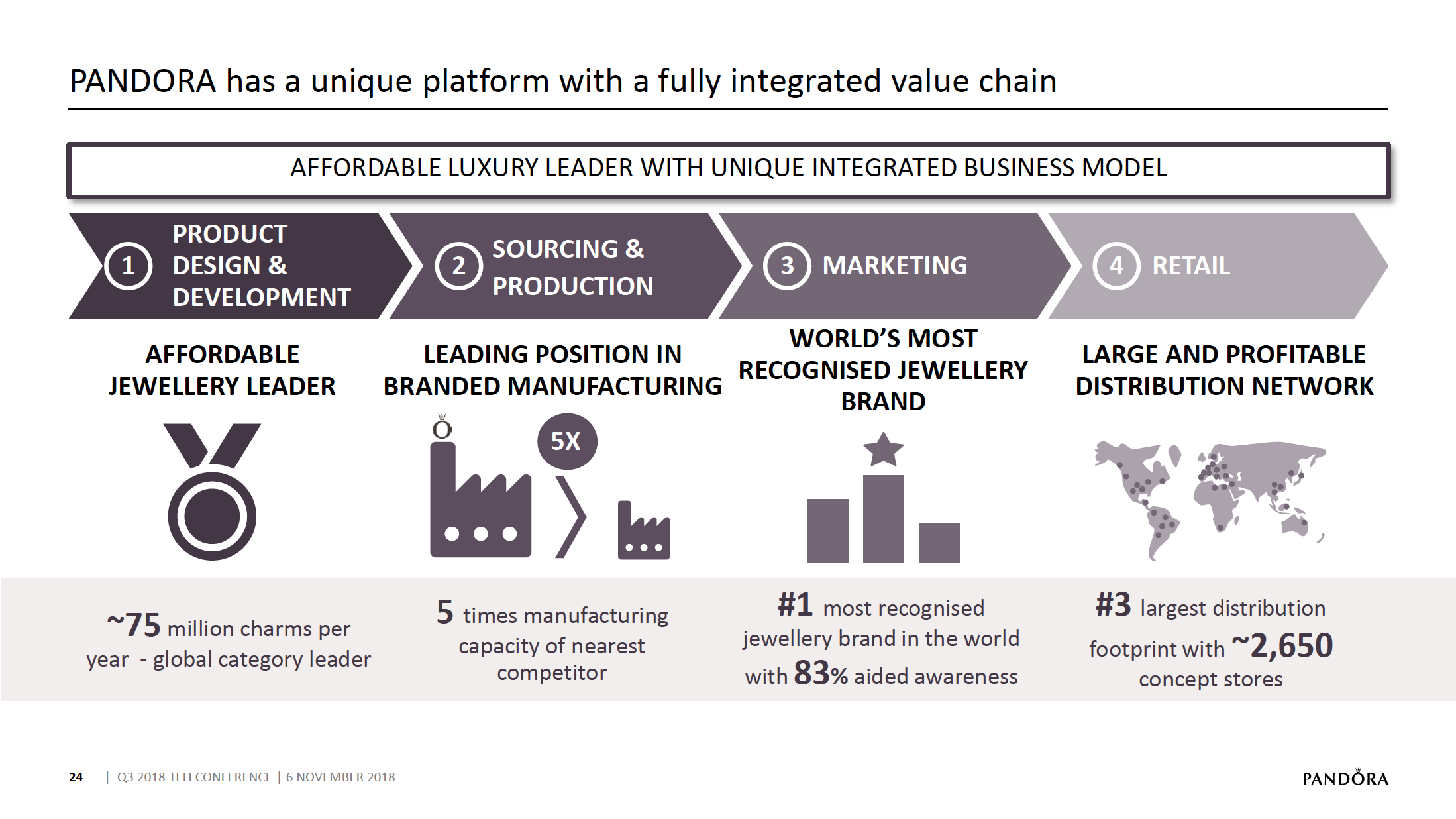

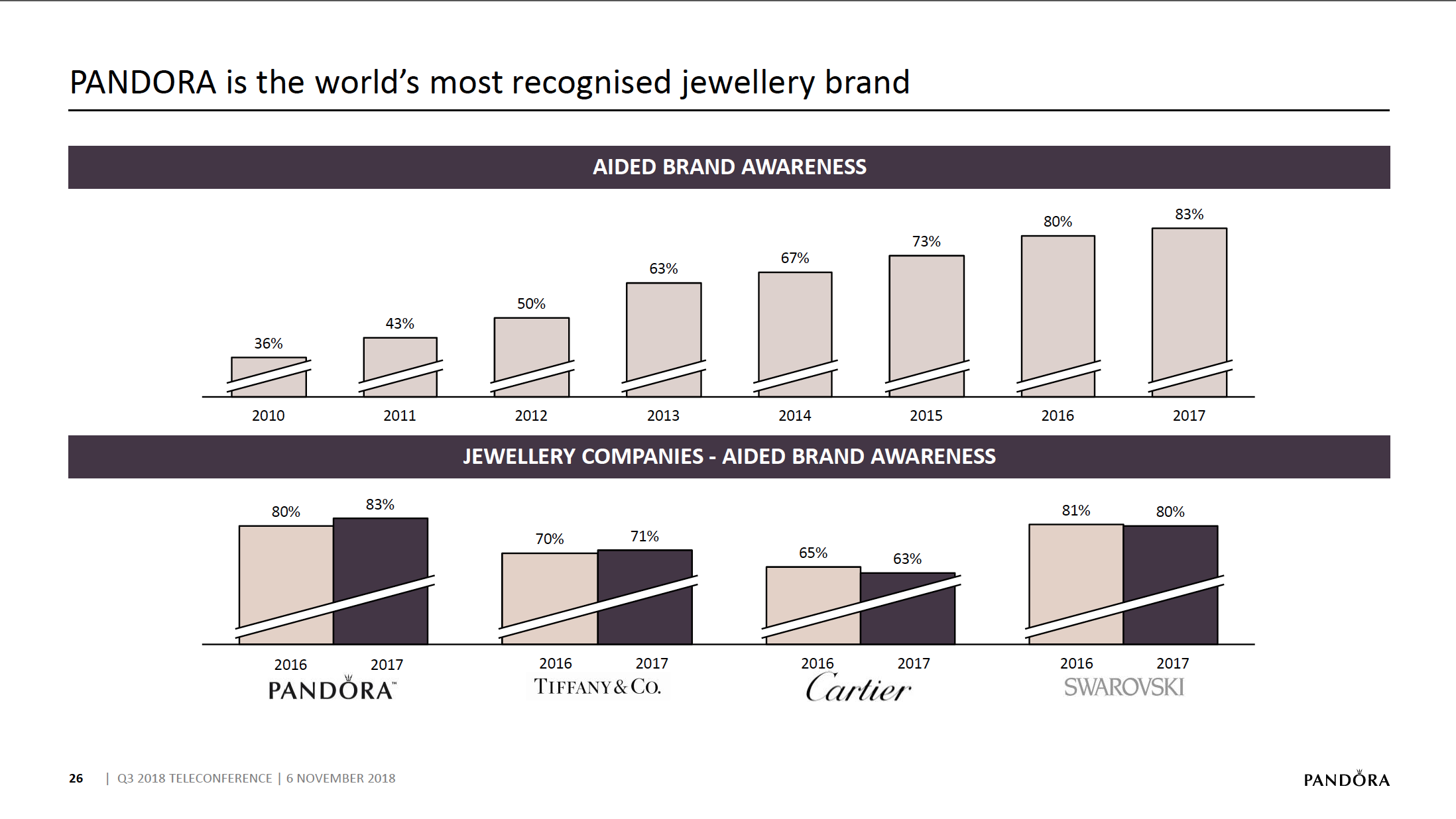

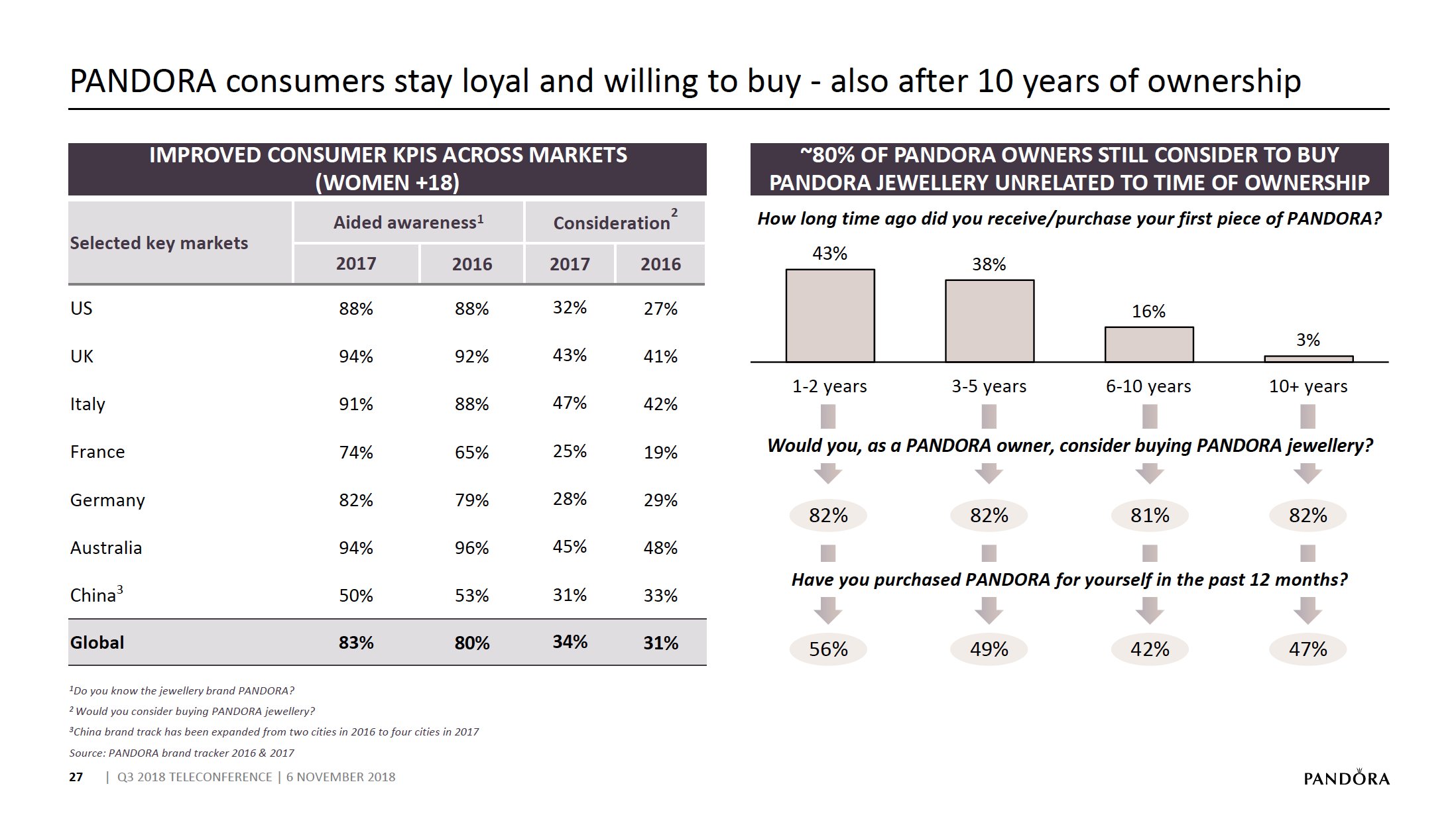

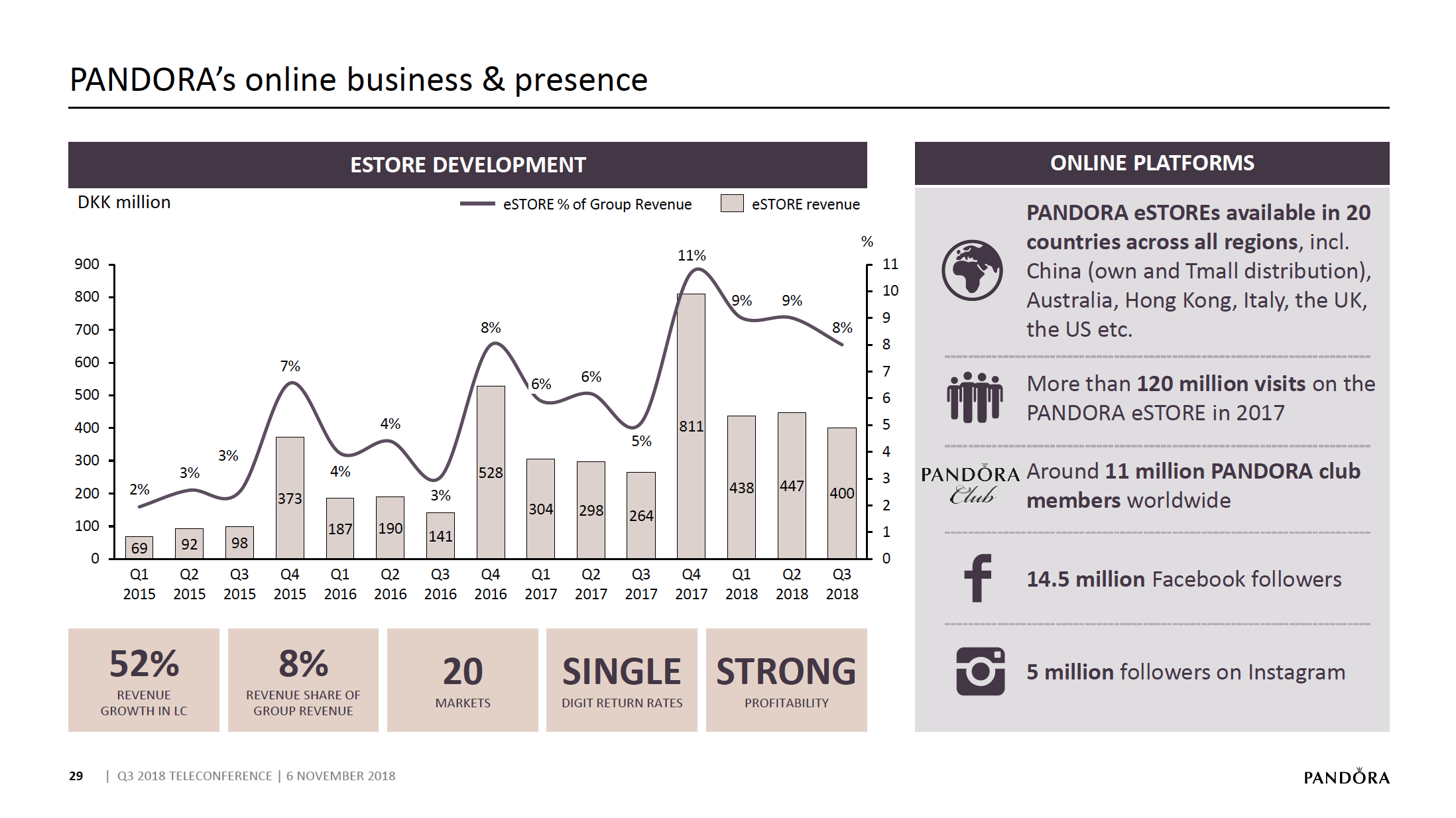

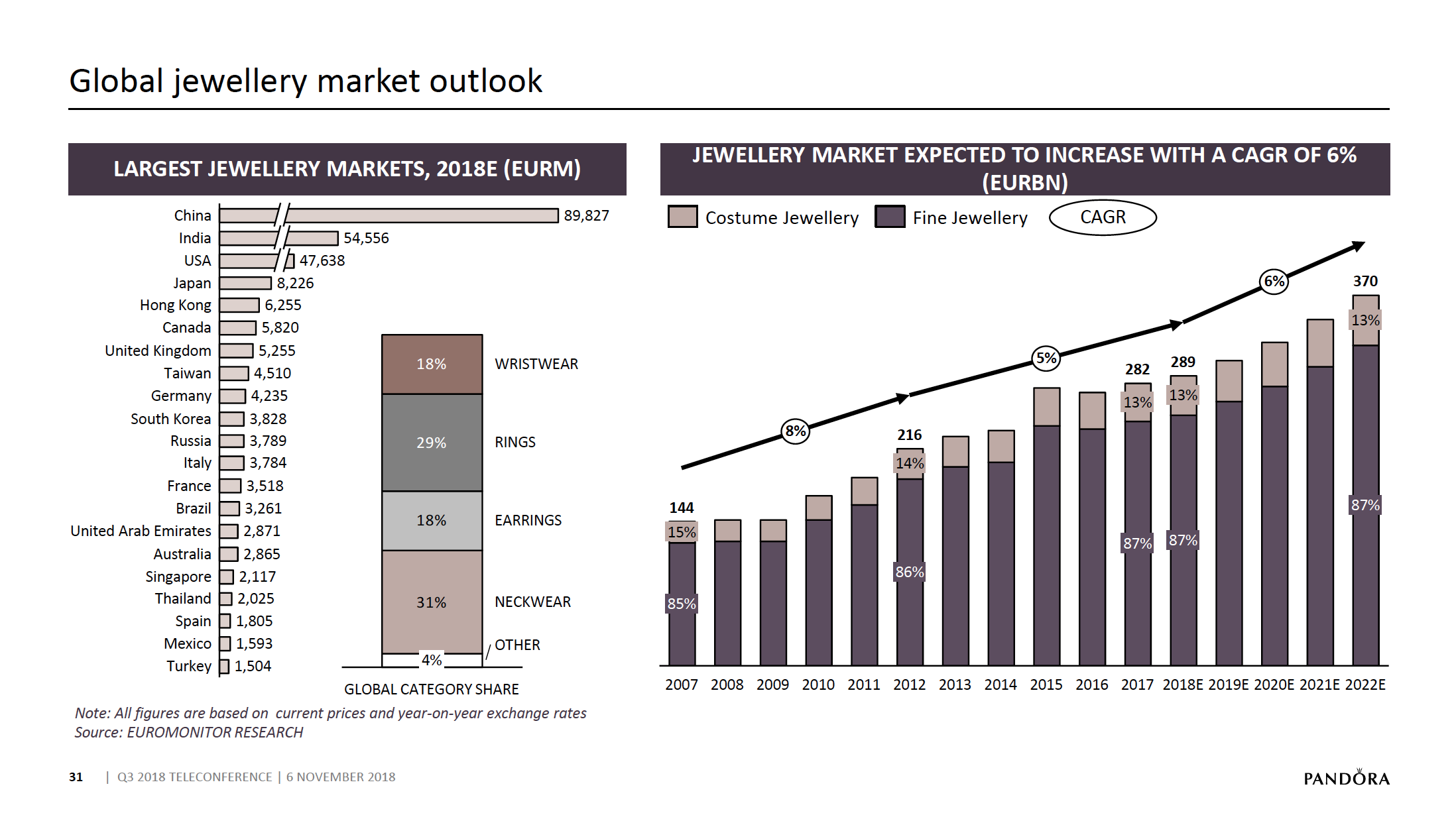

In summary it was a terrible quarter. Is it all bad then? No, online sales are improving, it is the best recognised jewelry brand in the world, they have a loyal customer base and the global jewelry market will not stop growing. But the days of rapid expansion and reliable double digit growth are probably permanently over.

Pandora remains attractively valued in absolute terms and relative to its peers. Their margins are still impressive in comparison with other manufacturers of luxury goods. And their cash flow still supports a generous buyback programme of DKK4b at somewhat depressed prices. But another negative earnings surprise in Q4 could easily send the share price further tumbling. Poor Q4 results in February and the arrival of a new CEO wanting to throw in the kitchen sink might prove to provide the perfect buying opportunity at further depressed price levels.