Teva reported on their first quarter results and issued the following press release with the following headlines and statements from the CEO:

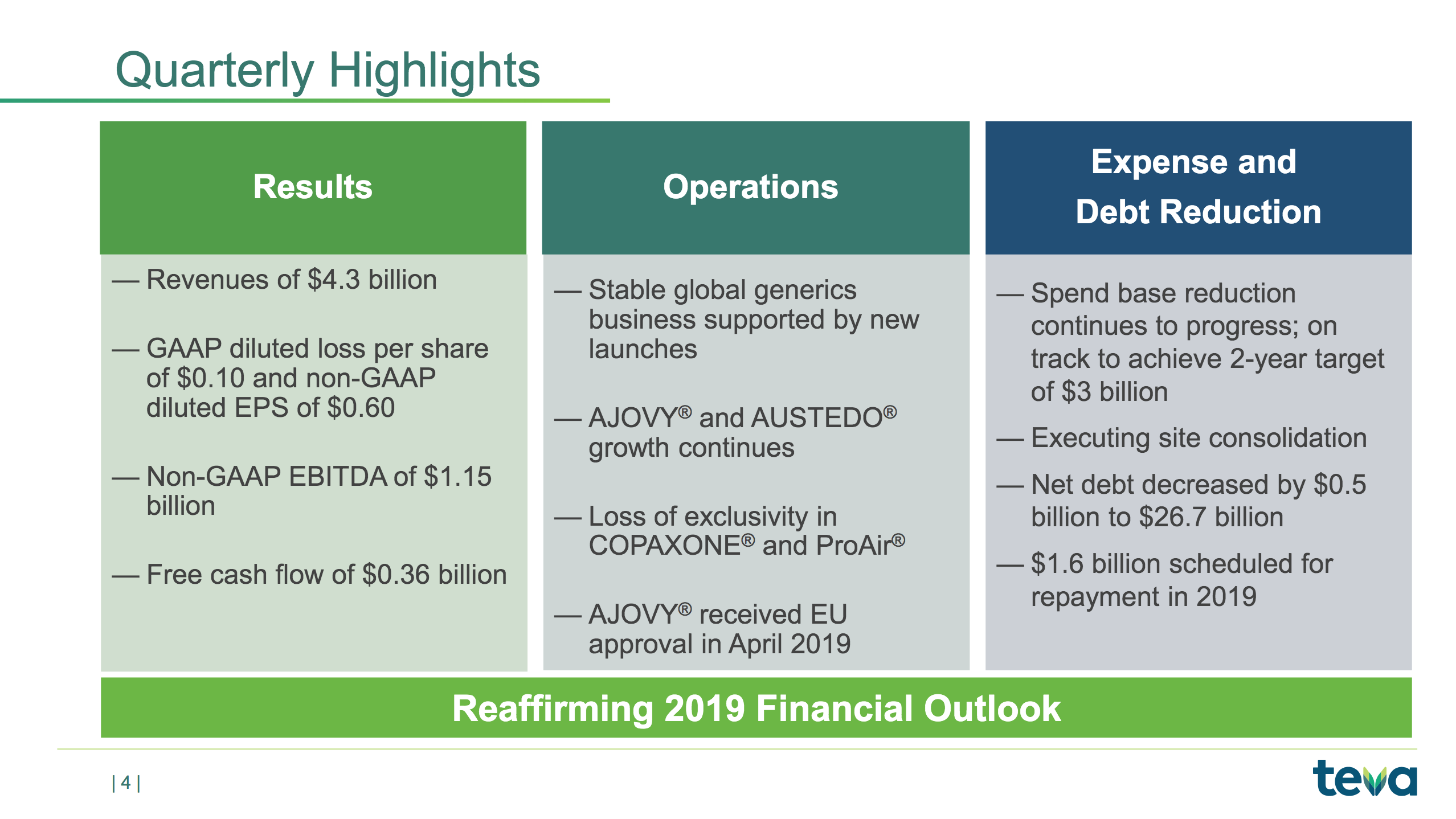

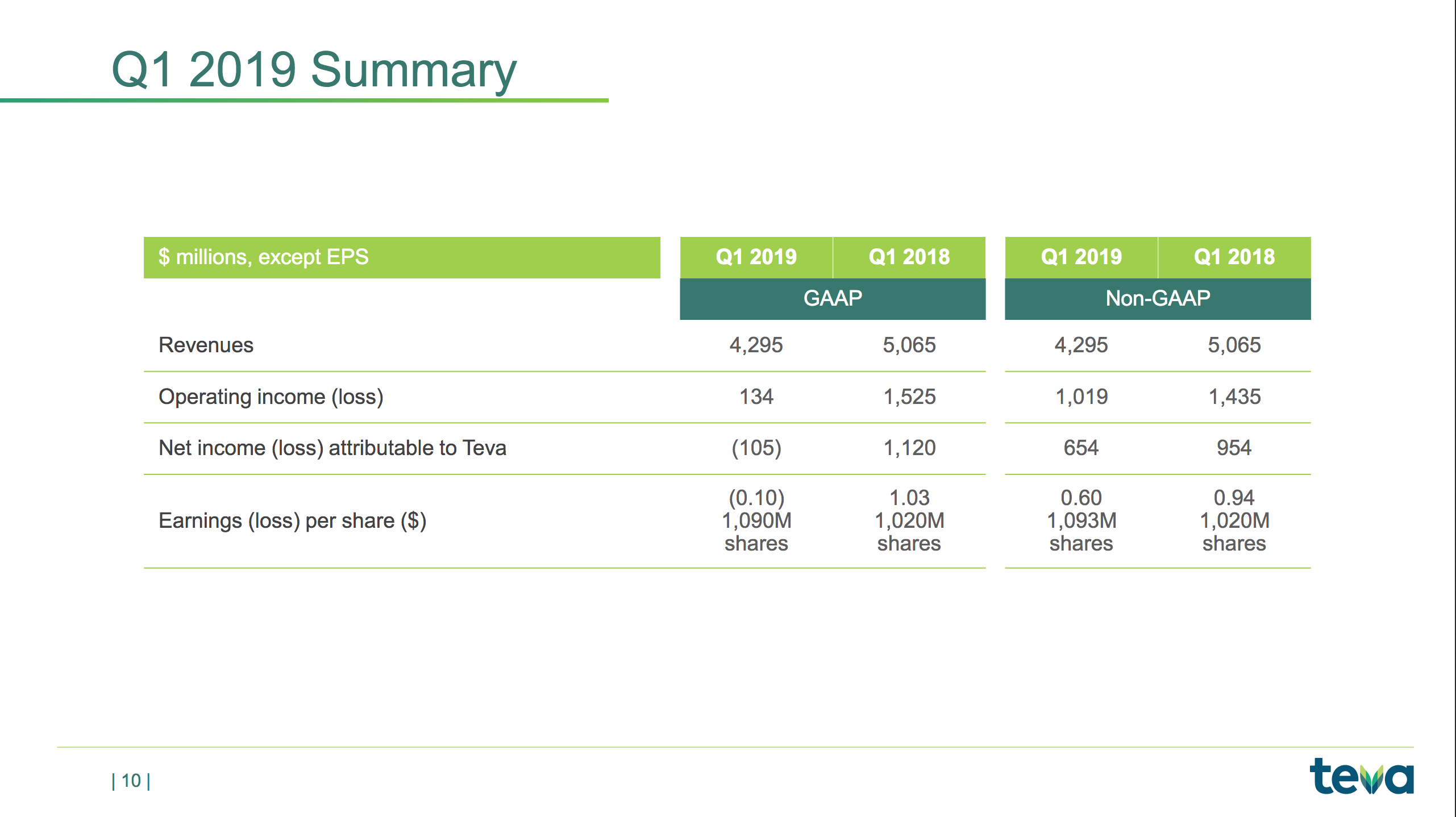

– Revenues of $4.3 billion

– GAAP diluted loss per share of $0.10

– Non-GAAP diluted EPS of $0.60

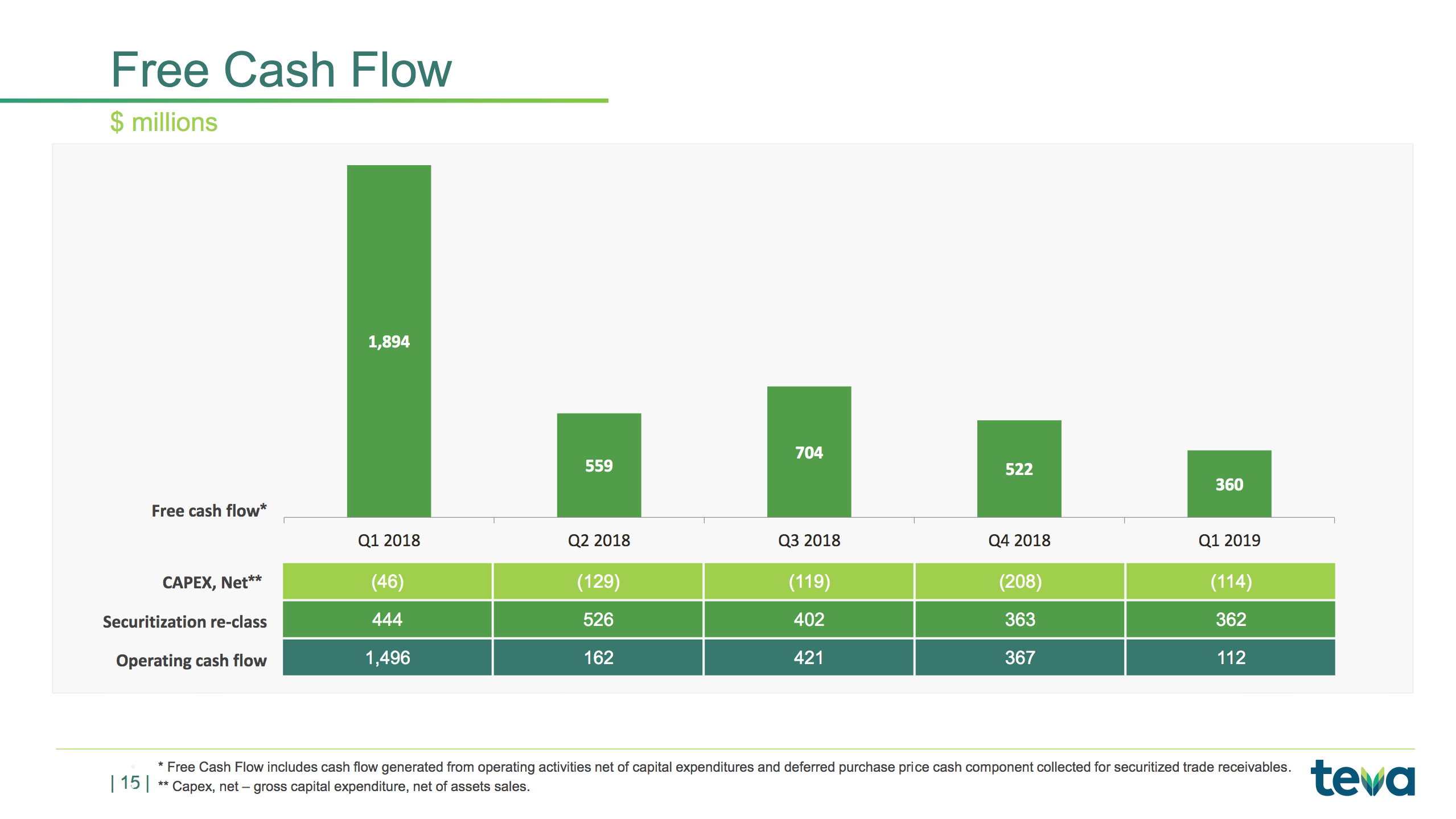

– Free cash flow of $360 million

– Spend base reduction of $2.5 billion since initiation of the – restructuring plan in 2018; on-track to achieve $3.0 billion by the end of 2019

– Full year 2019 revenues and EPS guidance reaffirmed

Mr. Kåre Schultz, Teva’s President and CEO, said, “The second year of our two-year restructuring program got off to a promising start. We are on track to reduce our total cost base by $3 billion by the end of 2019 and we have achieved a reduction of $2.5 billion to date, while continuing to lower our debt. “

Mr. Schultz continued: “We faced the expected loss of exclusivities of key products COPAXONE® and ProAir® to generic competition. Our focus is on stabilizing our global generics business and ensuring the success of our long-term organic growth drivers, especially AJOVY® and AUSTEDO®. Both products continue to gain momentum since their initial launches and we are making the necessary investments to be able to bring them to markets outside of the U.S. as well as explore additional indications.”

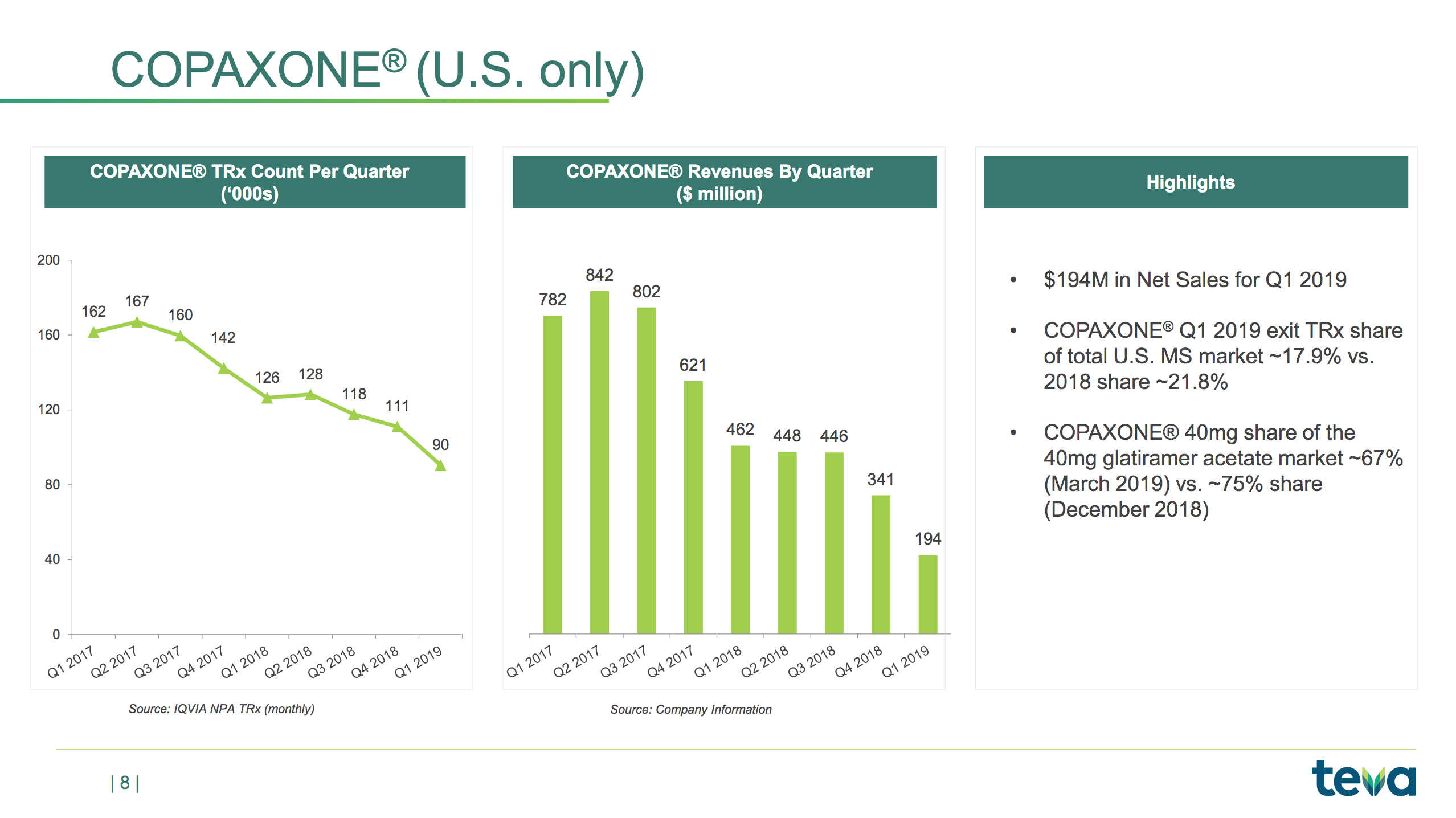

Below the revenue is shown for each geographic segment, the multiple sclerosis drug Copaxone® and generic drugs. The operating expenses are also shown.

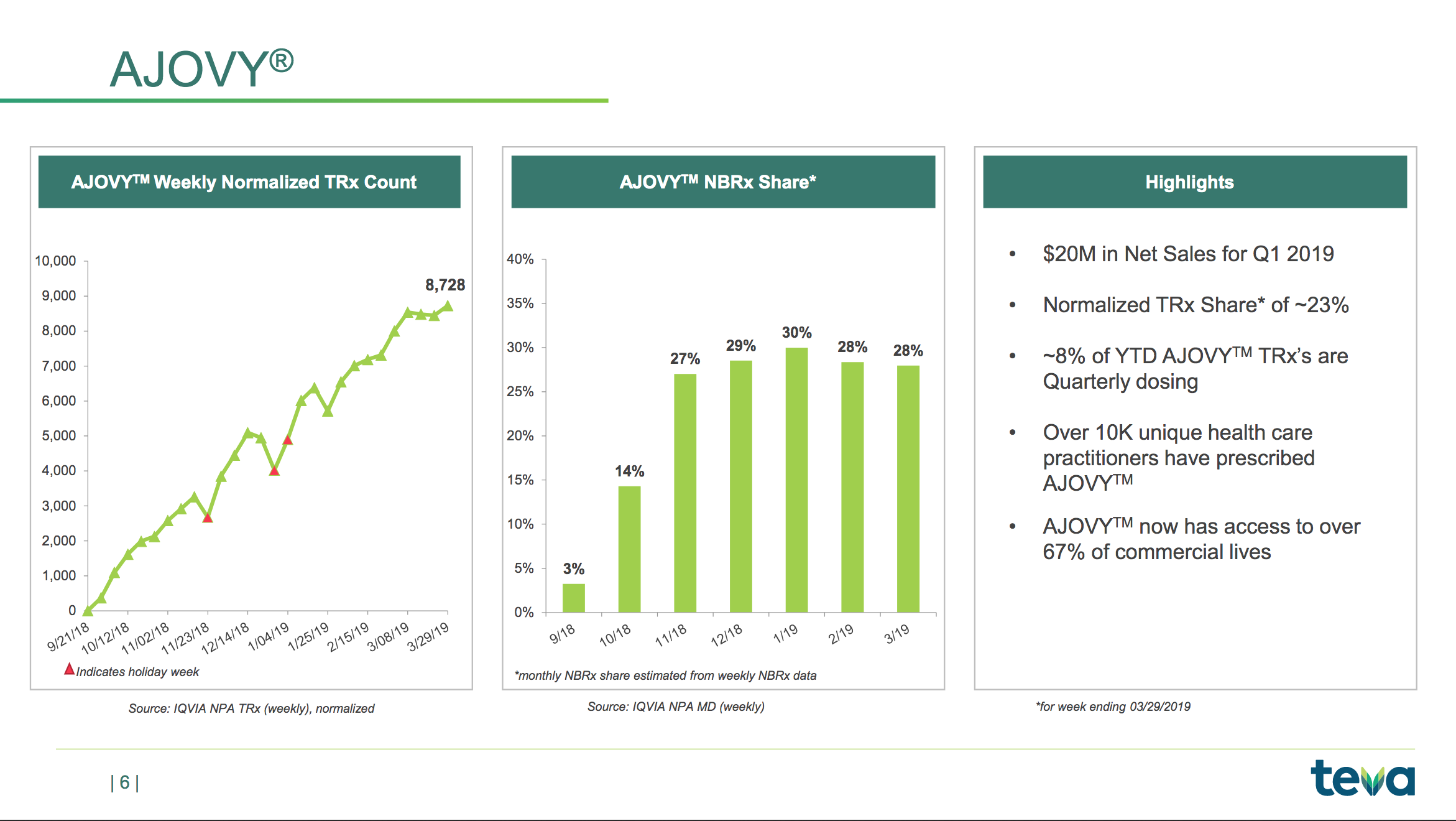

Copaxone® revenue has been further reduced following the introduction of generic versions from Mylan and Momenta at lower prices. Revenue from generic drugs in the US seems to have stabilised. The company is on track to achieve the goal of reducing expenses by $3B annually and $750M quarterly. The migraine drug Ajovy® does not yet contribute significantly to the overall revenue. Annual peak sales have been estimated to be greater than $500M. Ajovy® received EU approval in April 2019.

The slide below is a summary of the quarterly highlights not already mentioned above.

The slide below shows the NBRx market share of the migraine drug Ajovy®.

The current competition is Aimovig® from Amgen and Emgality® from Lilly.

Alder BioPharmaceuticals also has a CGRP migraine drug (eptinezumab) in phase 3.

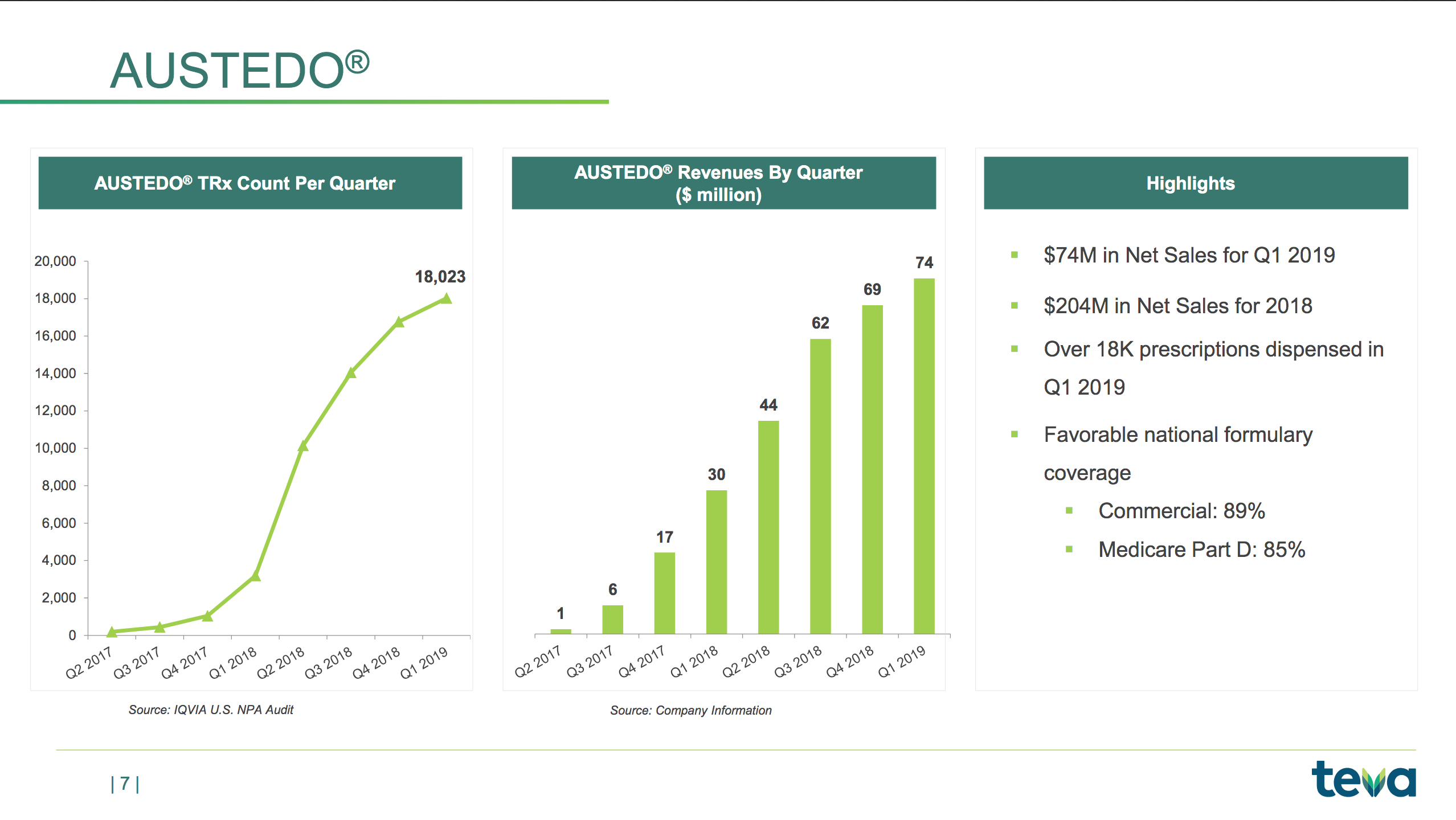

The slides below are summaries of Austedo®, Copaxone® and Ajovy®

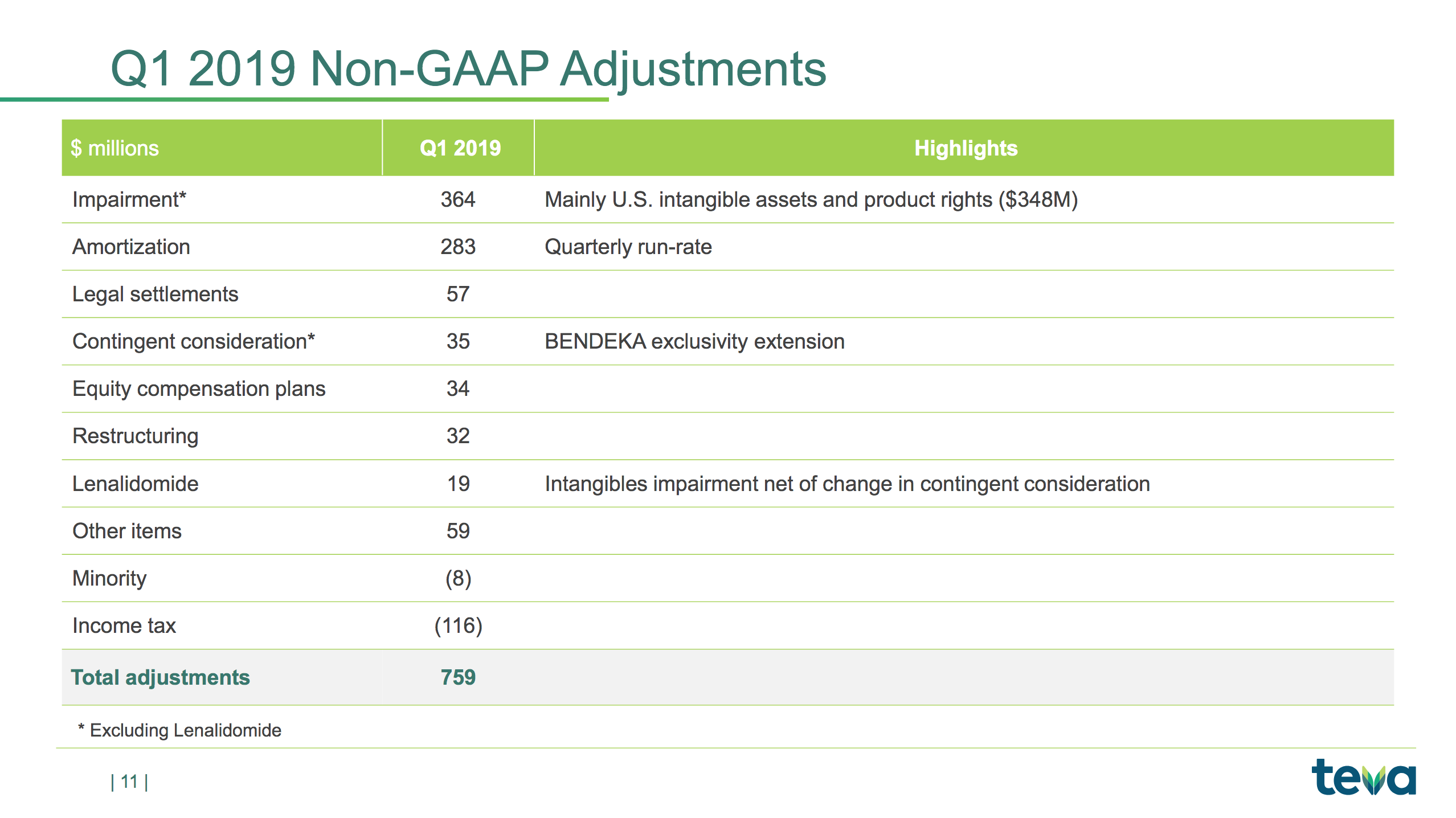

The slides below are summaries of GAAP and non-GAAP metrics and a summary of the items causing the difference; e.g. $348M of impairment charges to intangible assets and amortisation of $283M.

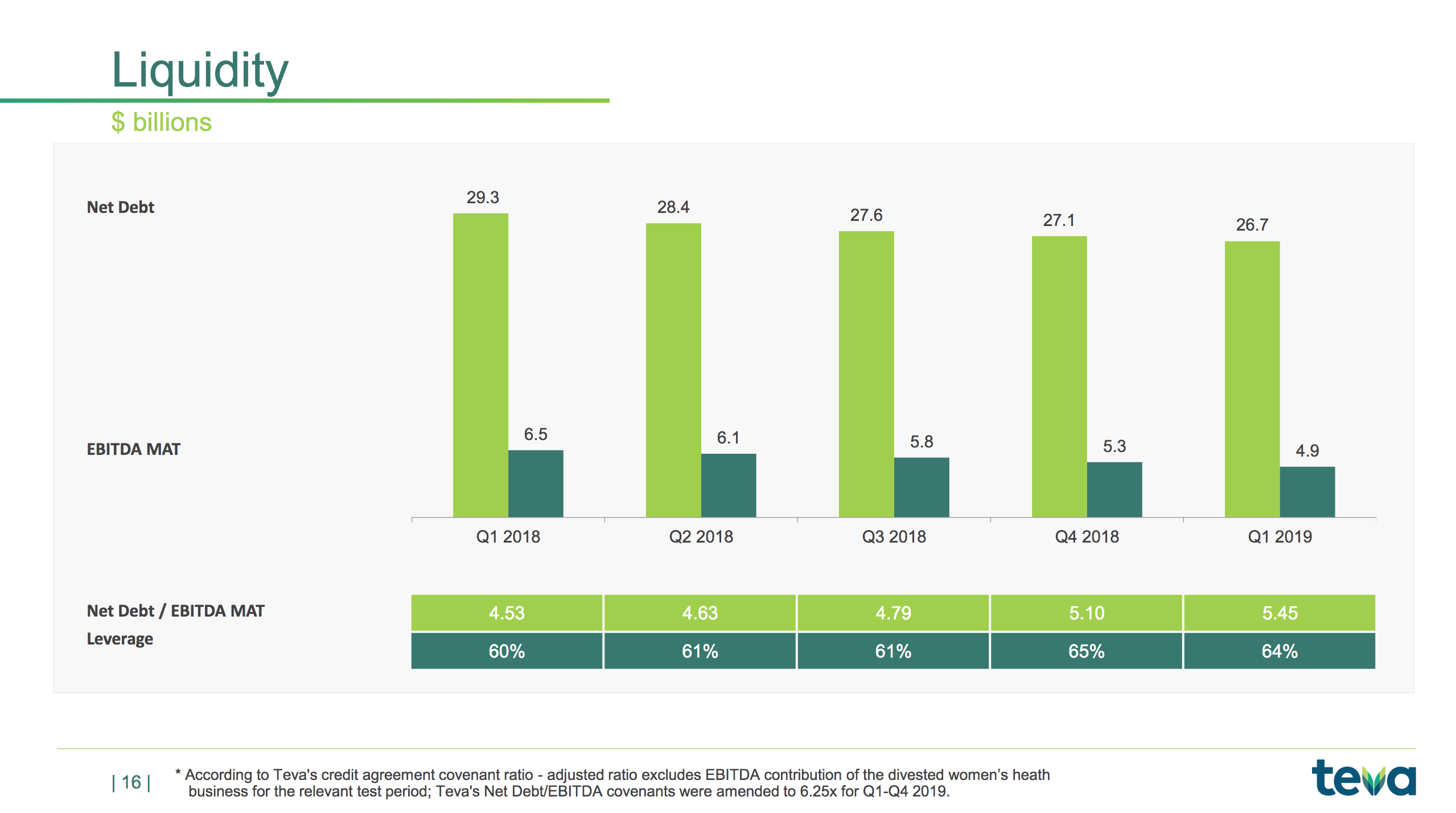

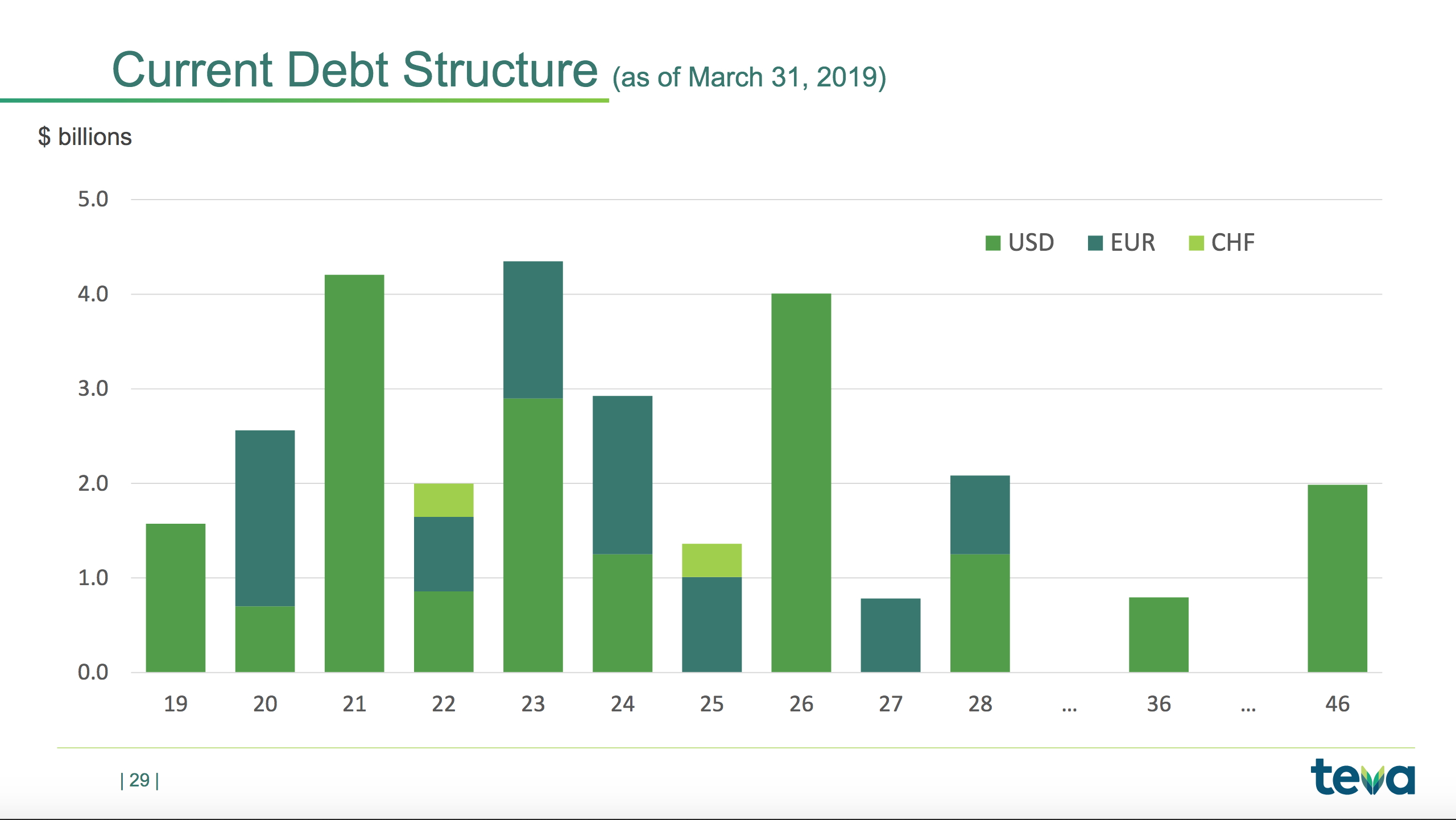

The slides below summarises the free cash flow and the long term debt.

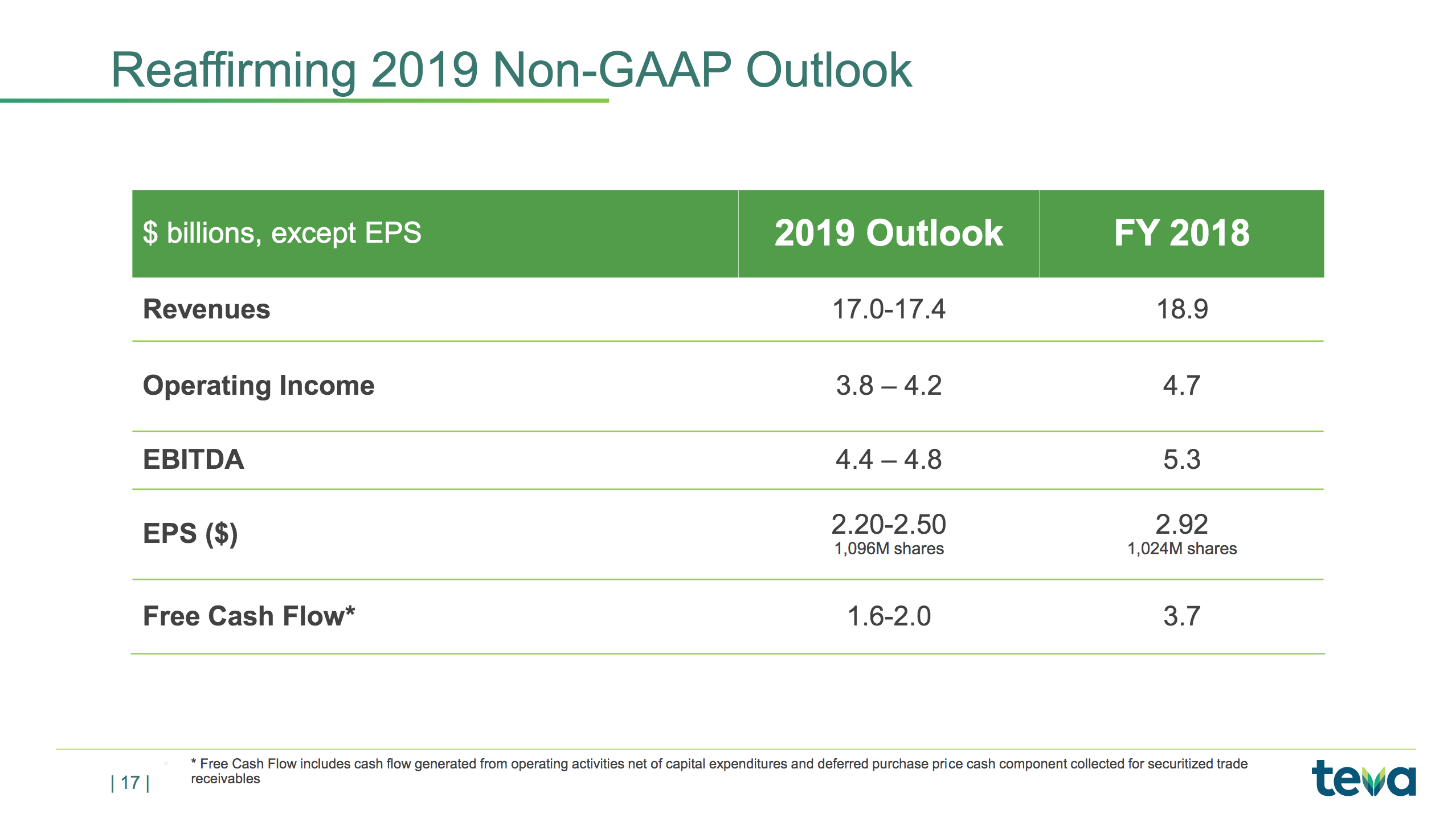

The slide below summarises the non-GAAP outlook.

The final slide below shows the debt maturity. The CEO has said the company will not need to raise equity, but given the reduced revenue, profit and cash flow the company will definitely have to refinance. Currently the credit rating is BB with S&P and Ba2 with Moody’s.

I do think Teva could trade close to $30 within the next 2-5 years, but it’s not a business I would own long term, so I choose not to buy at $14-16 despite the lowest EPS forecast for 2020 currently being $2.28 and the remainder of the market (i.e. S&P500) being somewhat overpriced.

During the call the CEO didn’t reveal much about the long term targets and long term strategy:

Yeah, of course, we have the aim to become as effective as any of our competitors, which means that longer-term we need to improve our margins which is why we have a long-term financial target of an operating margin of 27%, which is higher than where we are right now. So, of course, in order to achieve that, we need to set plans in place so that this happens. Our plan right now is to communicate more broadly on this once we finish this year. So once we finish the restructuring of ’18 and ’19, we will communicate to you what is our strategy for manufacturing and for that part of the cost base.

You can see that, we have a long-term target of the operating profit of 27%, that’s higher than where we are now. Part of that improvement of course has to come from the COGS, because if we don’t improve the gross margin, then it’s going to be very difficult to get a significant improvement of the total margin. So yes, we will be targeting something like that. We will give you some more details on what we are planning to do once we finish the restructuring, that means once we report on the full year of 2019. Next February, we’ll give you an outline of how we see the ongoing optimization of our manufacturing system.

On the R&D side, we spent roughly $1 billion on R&D, and you could see the — a big chunk of that is for innovative specialty products. We have about 30 development projects ongoing, about two-thirds of those are biopharmaceuticals. And we don’t really want to share that with anybody right now. The reason is that, we are in the restructuring right now this year and last year, but our plan is to share more with you once we finish this year. So once we get to February of next year, we will share a bit more with you on what is our pipeline, what are the different projects we have.

Globes, May 2nd: Teva Q1 revenue down but profit beats analysts

Bloomberg, May 2nd: Teva Falls as Sales of Copaxone Decline Faster Than Expected

Reuters, May 2nd: Teva’s new migraine drug helps to contain profit fall

Globes, May 3rd: Teva CEO unsure about 2020 growth

CNBC, May 5th: Migraine drugs cause pain for investors