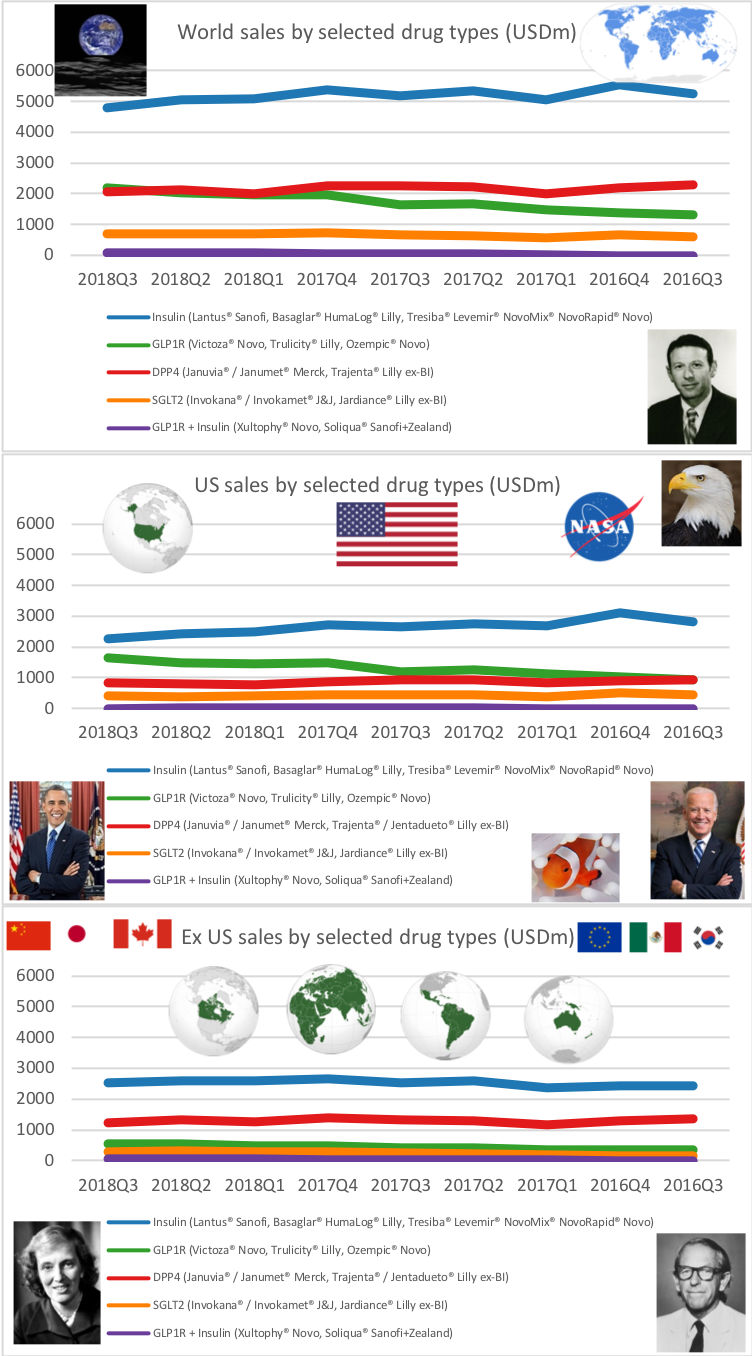

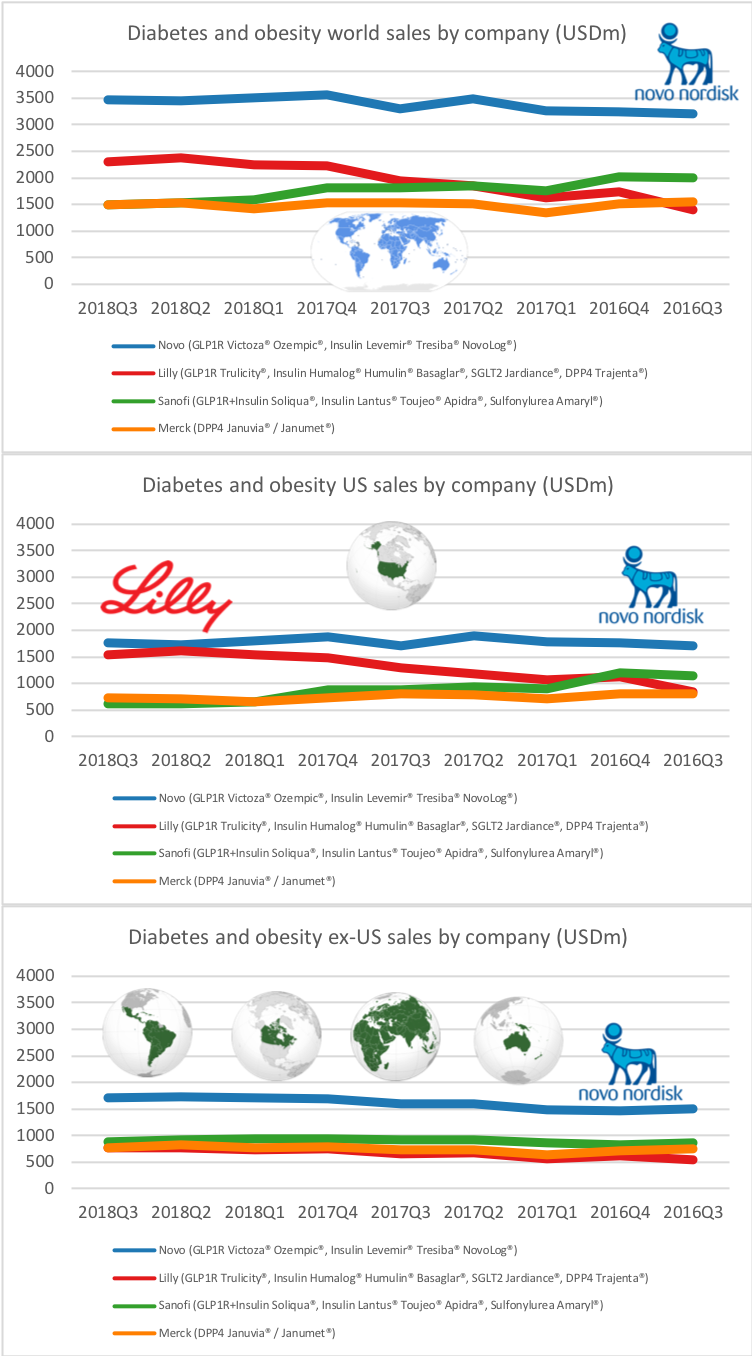

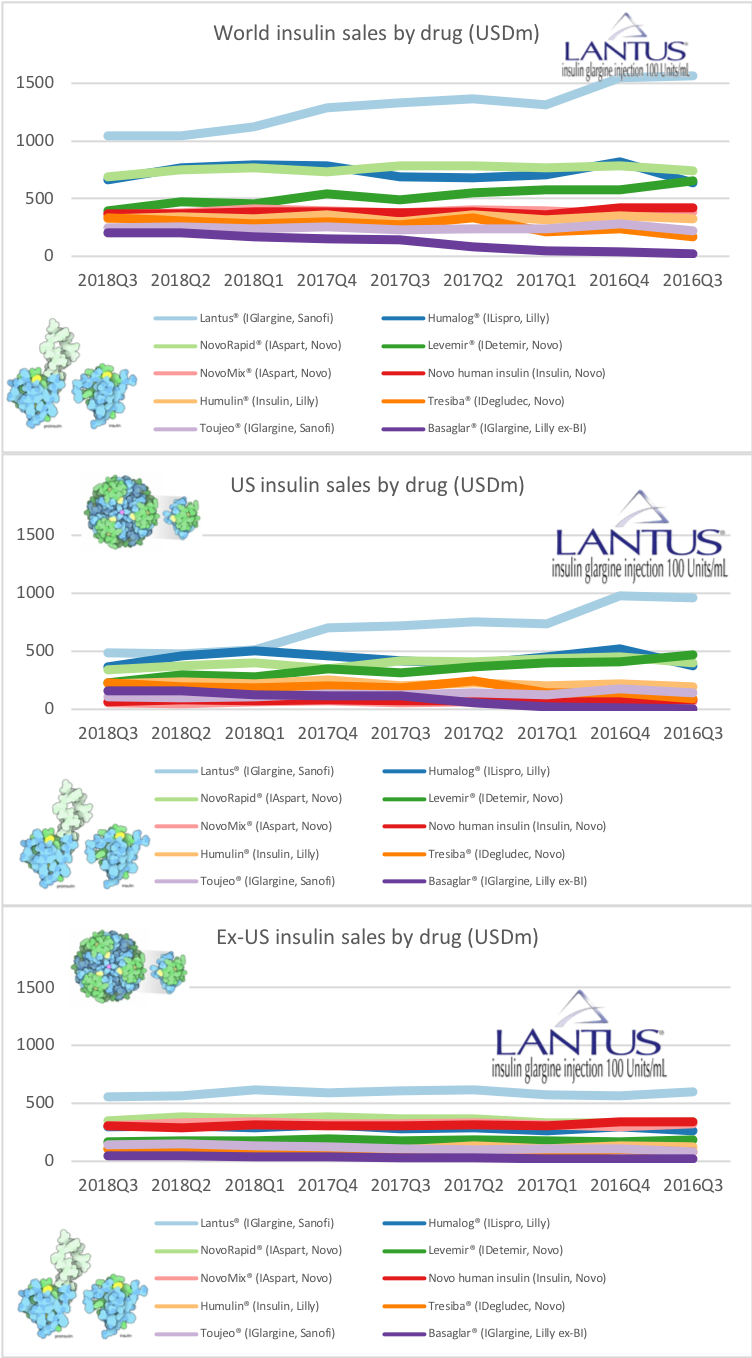

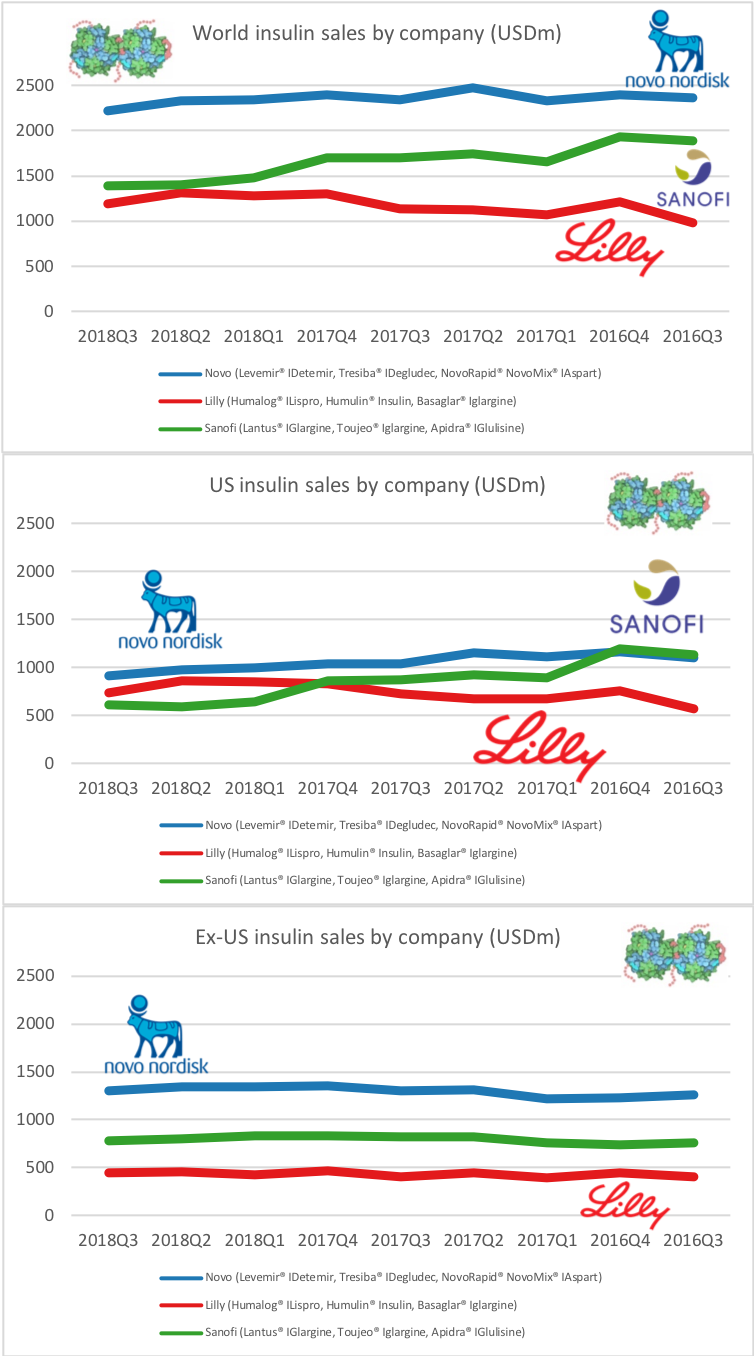

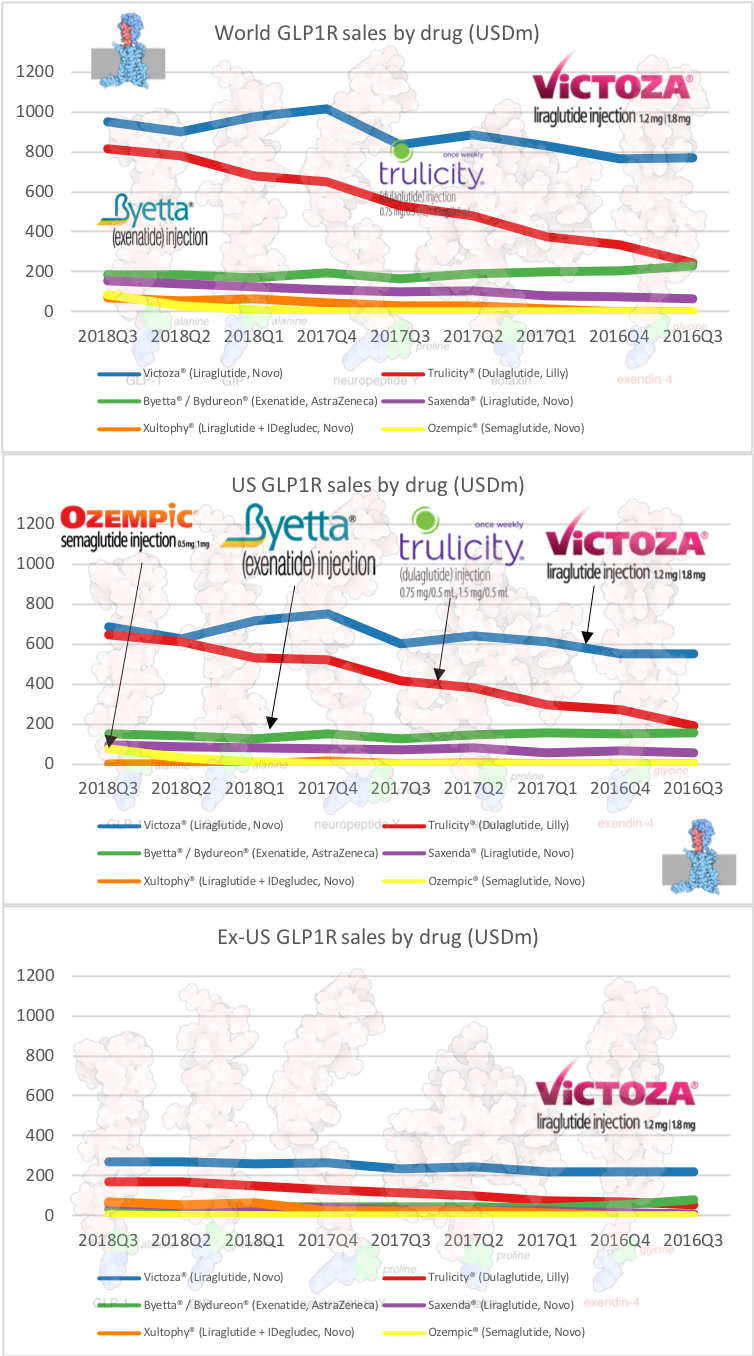

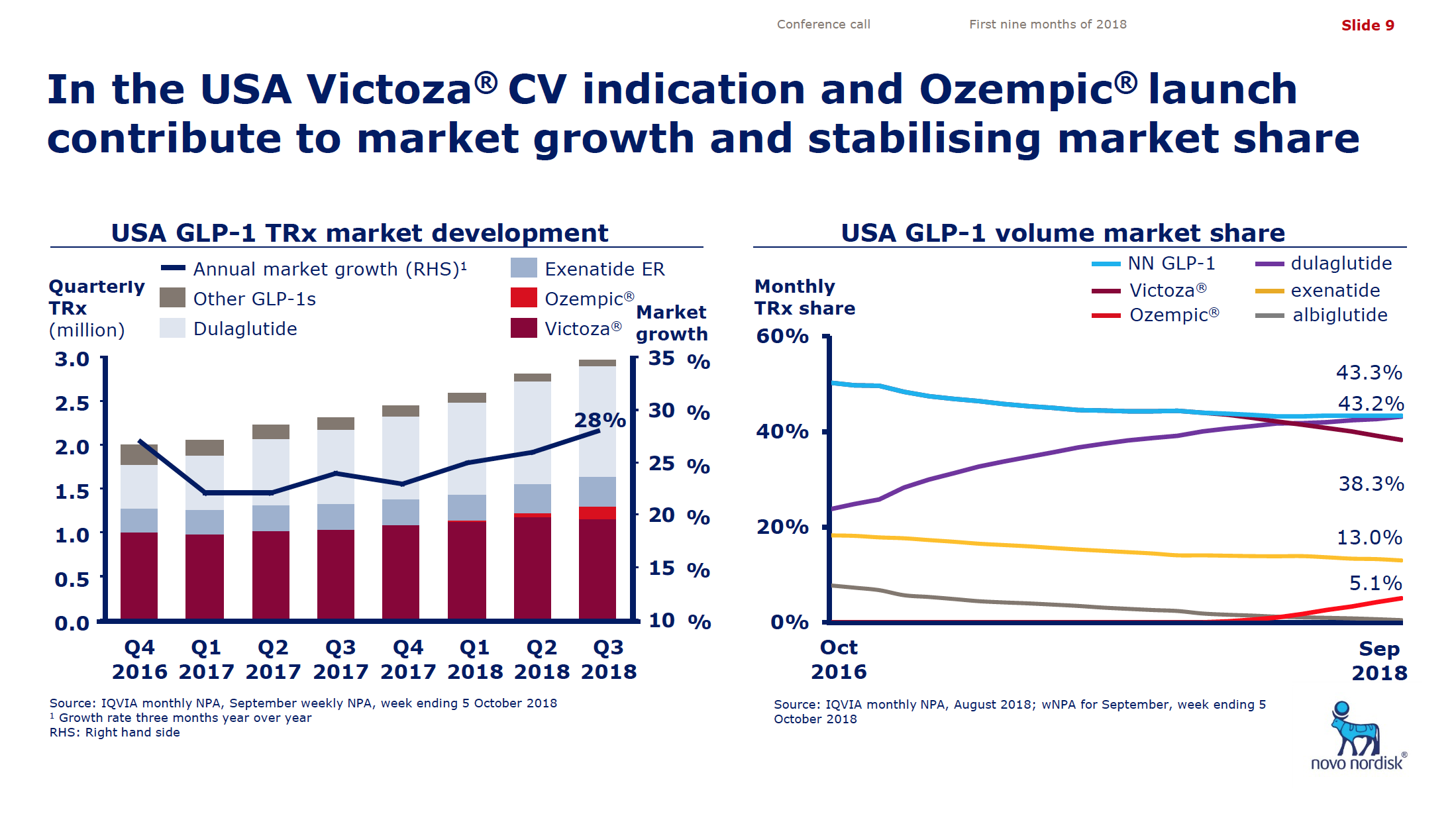

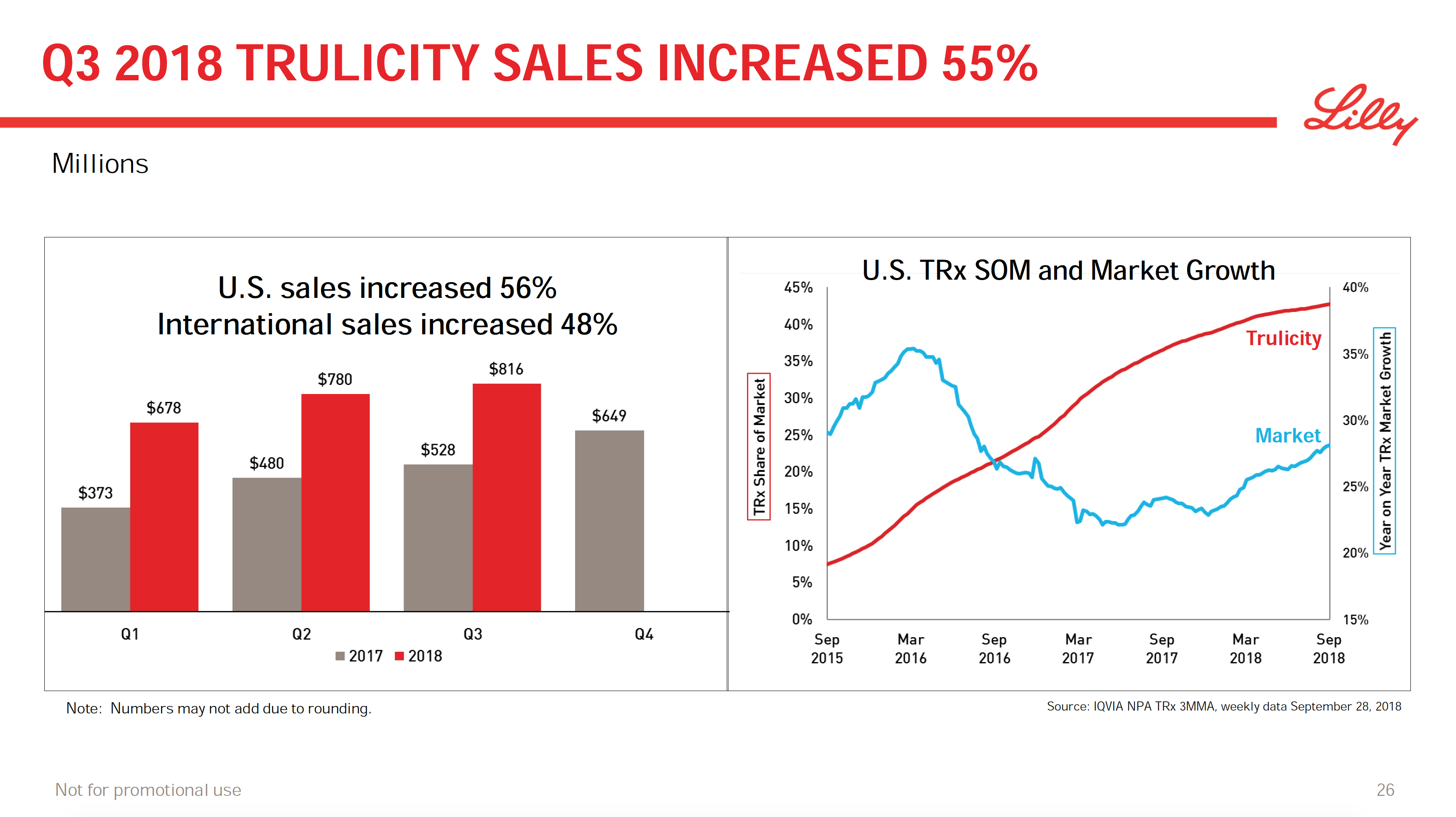

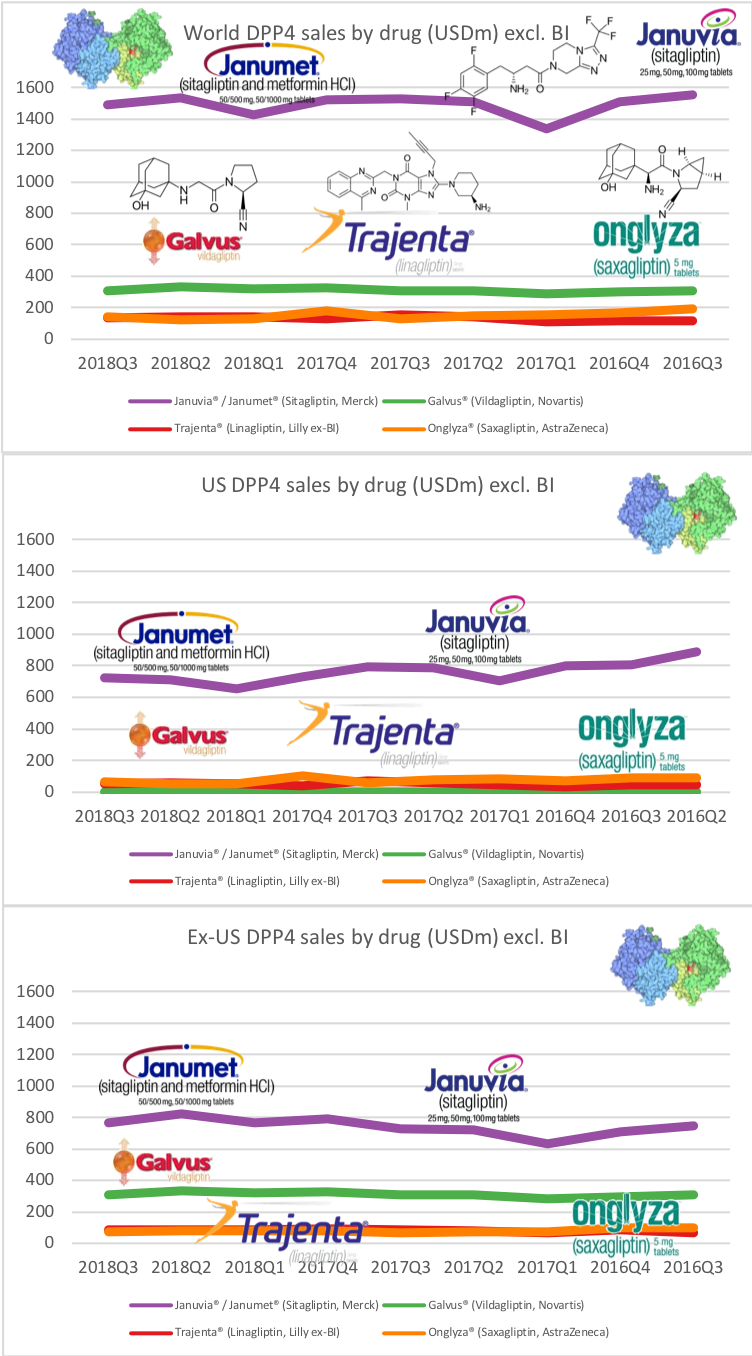

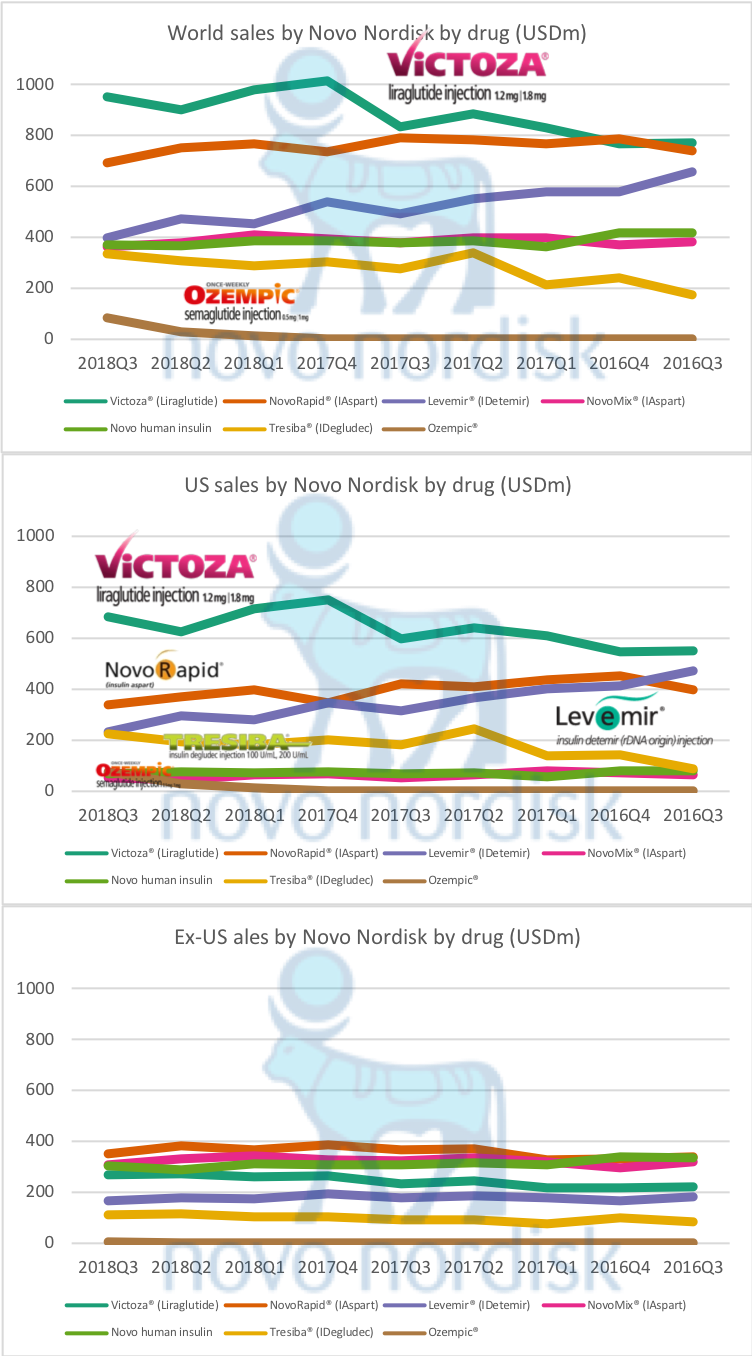

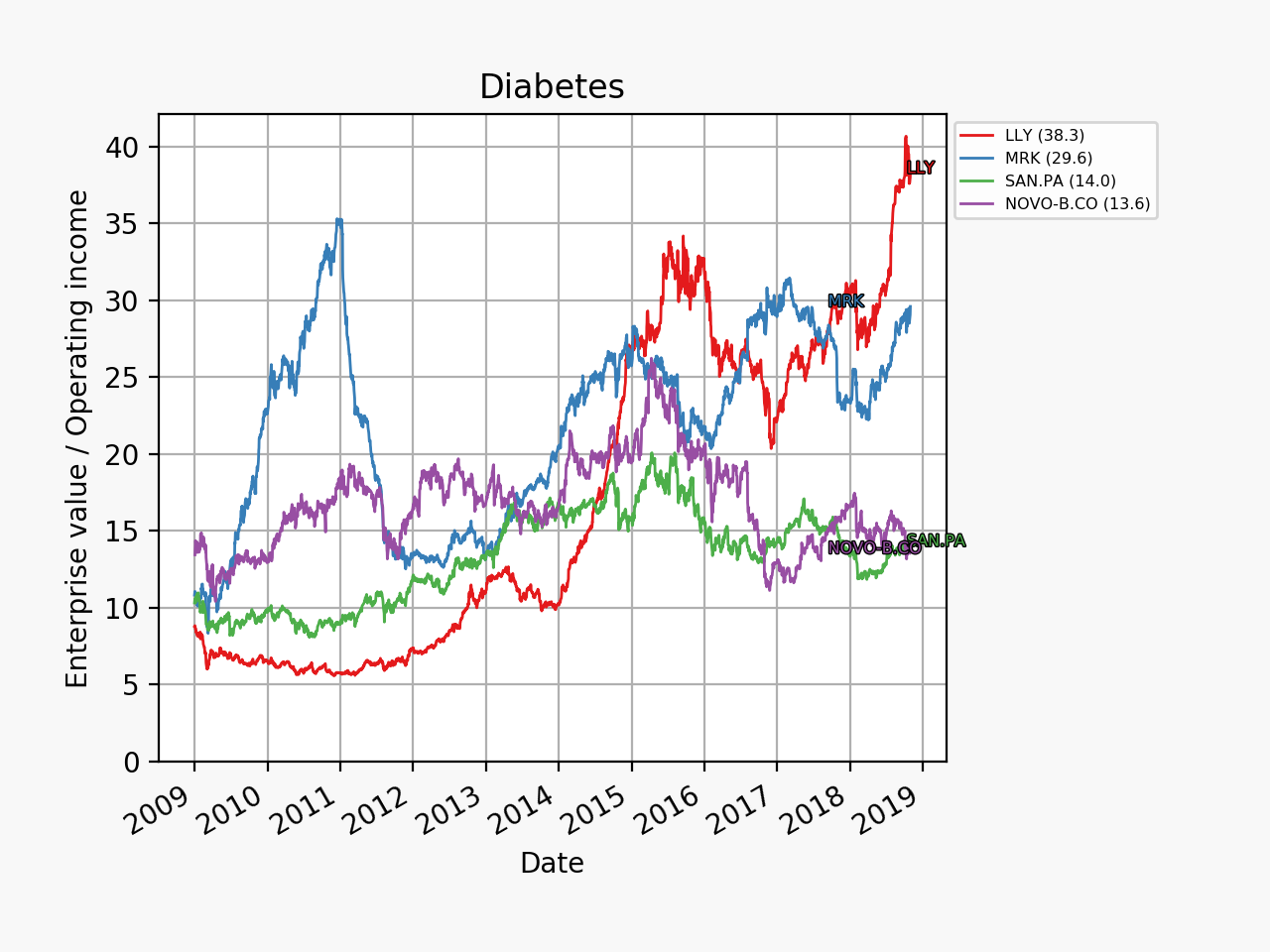

Novo Nordisk has released their annual report. Positive growth was driven primarily by Ozempic® in the US, Saxenda®, Tresiba® and Victoza®, whereas negative growth was driven by primarily Levemir® in the US. The mentioned drugs and the trailing twelve month (TTM) sales of diabetes and obesity drugs are summarised below.

| Name | Drug | Type | Injection | Therapy | Successor |

|---|---|---|---|---|---|

| Ozempic® | Semaglutide | GLP-1 | Weekly | Diabetes | – |

| Victoza® | Liraglutide | GLP-1 | Daily | Diabetes | Ozempic® |

| Saxenda® | Liraglutide | GLP-1 | Daily | Obesity | semaglutide? |

| Tresiba® | InsDegludec | Insulin | Once daily | Diabetes | LAI287? |

| Levemir® | InsDetemir | Insulin | Once or twice daily | Diabetes | Tresiba® |

| Xultophy® | InsDegludec + Liraglutide | Insulin + GLP-1 | Once daily | Diabetes | LAIsema? |

| NovoRapid® | InsAspart | Insulin | – | Diabetes | – |

| NovoMix® | InsAspart | Insulin | – | Diabetes | – |

| Ryzodeg® | InsAspart + InsDegludec | Insulin | – | Diabetes | – |

| Fiasp® | InsAspart | Insulin | – | Diabetes | – |

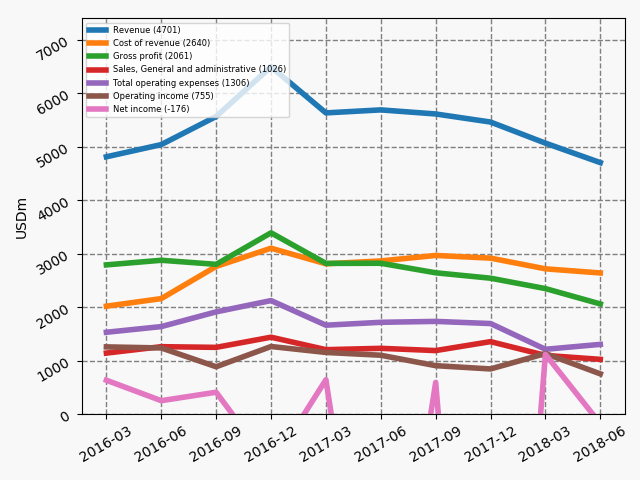

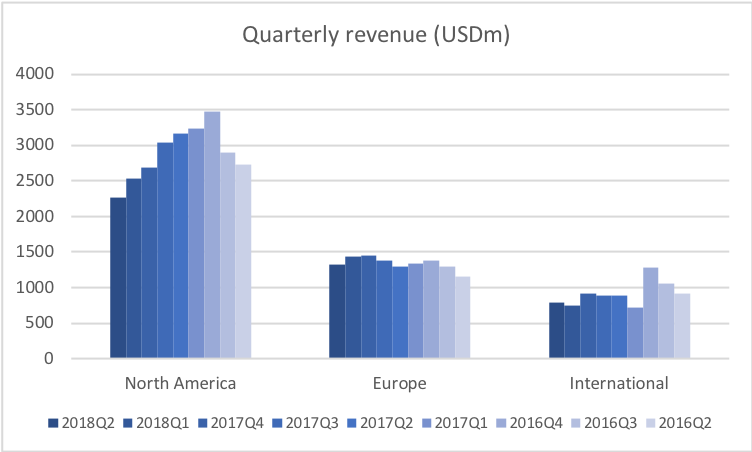

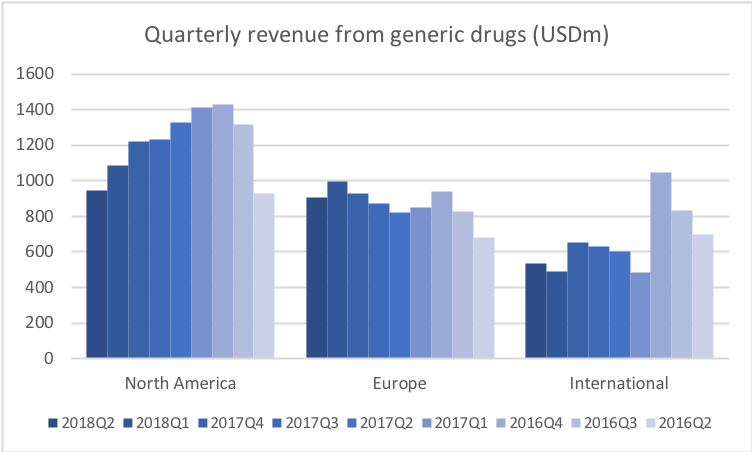

Business segments

The revenue and profit generated by the two business segments and is summarised below:

R&D

In terms of R&D highlights they were LAI287 and the completion of the PIONEER6 phase 3 study on oral semaglutide. The slide below summarises other highlights:

On November 23rd Novo Nordisk sent out a press release on the PIONEER6 results, which concluded the PIONEER studies on oral semaglutide:

Oral semaglutide demonstrates favourable cardiovascular safety profile and significant reduction in cardiovascular death and all-cause mortality in people with type 2 diabetes in the PIONEER 6 trial

The result of the PIONEER studies in terms of HbA1c reduction and weight loss is summarised in the figure below:

[expand title=”Click for links to all of the press releases on the PIONEER trials:”]

PIONEER 1:

Efficacy and Safety of Oral Semaglutide Versus Placebo in Subjects With Type 2 Diabetes Mellitus Treated With Diet and Exercise Only (PIONEER 1)

https://clinicaltrials.gov/ct2/show/NCT02906930

Novo Nordisk successfully completes the first phase 3a trial, PIONEER 1, with oral semaglutide

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2170941.html

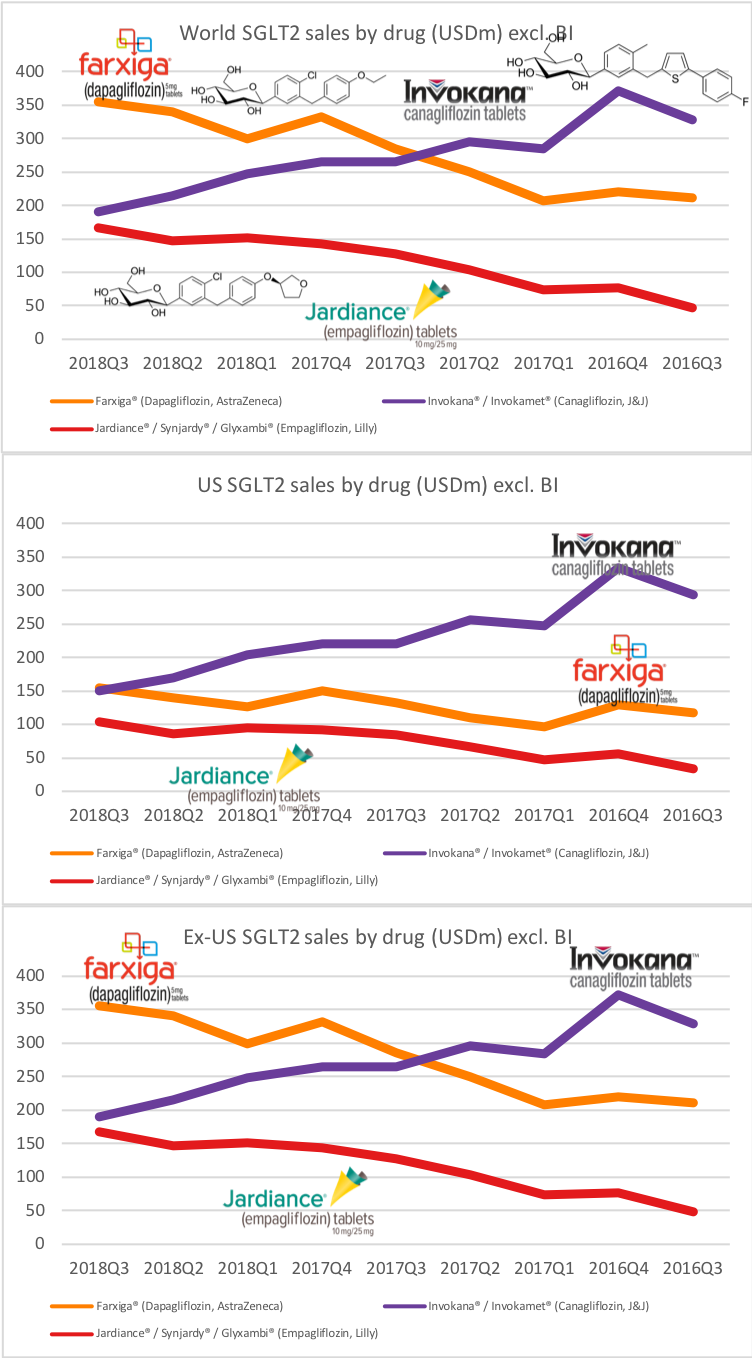

PIONEER 2 (vs SGLT2 / Jardiance® from Lilly):

Efficacy and Safety of Oral Semaglutide Versus Empagliflozin in Subjects With Type 2 Diabetes Mellitus (PIONEER 2)

https://clinicaltrials.gov/ct2/show/NCT02863328

Oral semaglutide shows superior improvement in HbA1c vs empagliflozin in the PIONEER 2 trial

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2195846.html

PIONEER 3 (vs DPP4 / Januvia® from Merck):

Efficacy and Long-term Safety of Oral Semaglutide Versus Sitagliptin in Subjects With Type 2 Diabetes (PIONEER 3)

https://clinicaltrials.gov/ct2/show/NCT02607865

Oral semaglutide shows superior reductions in HbA1c and weight compared to sitagliptin in the long-term safety and efficacy trial, PIONEER 3

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2211063.html

PIONEER 4:

Efficacy and Safety of Oral Semaglutide Versus Liraglutide and Versus Placebo in Subjects With Type 2 Diabetes Mellitus (PIONEER 4)

https://clinicaltrials.gov/ct2/show/NCT02863419

Oral semaglutide shows statistically significantly greater reductions in HbA1c and weight compared to Victoza® and sitagliptin in the PIONEER 4 and 7 trials

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2200408.html

PIONEER 5:

Efficacy and Safety of Oral Semaglutide Versus Placebo in Subjects With Type 2 Diabetes and Moderate Renal Impairment (PIONEER 5)

https://clinicaltrials.gov/ct2/show/NCT02827708

Oral semaglutide provides superior HbA1c and weight reductions versus placebo in people with type 2 diabetes and renal impairment in the PIONEER 5 trial

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2211959.html

PIONEER 6:

A Trial Investigating the Cardiovascular Safety of Oral Semaglutide in Subjects With Type 2 Diabetes (PIONEER 6)

https://clinicaltrials.gov/ct2/show/NCT02692716

Oral semaglutide demonstrates favourable cardiovascular safety profile and significant reduction in cardiovascular death and all-cause mortality in people with type 2 diabetes in the PIONEER 6 trial

https://www.novonordisk.com/media/news-details.2226789.html

PIONEER 7:

Efficacy and Safety of Oral Semaglutide Using a Flexible Dose Adjustment Based on Clinical Evaluation Versus Sitagliptin in Subjects With Type 2 Diabetes Mellitus. (PIONEER 7)

https://clinicaltrials.gov/ct2/show/NCT02692716

Oral semaglutide shows statistically significantly greater reductions in HbA1c and weight compared to Victoza® and sitagliptin in the PIONEER 4 and 7 trials

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2200408.html

PIONEER 8:

Efficacy and Safety of Oral Semaglutide Versus Placebo in Subjects With Type 2 Diabetes Mellitus Treated With Insulin (PIONEER 8)

https://clinicaltrials.gov/ct2/show/NCT03021187

Oral semaglutide demonstrates statistically significant reductions in HbA1c and body weight in people with long duration of type 2 diabetes treated with insulin

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2222176.html

PIONEER 9:

Dose-response, Safety and Efficacy of Oral Semaglutide Versus Placebo and Versus Liraglutide, All as Monotherapy in Japanese Subjects With Type 2 Diabetes (PIONEER 9)

https://clinicaltrials.gov/ct2/show/NCT03018028

Oral semaglutide demonstrates greater reductions in both HbA1c and body weight compared to Victoza® in Japanese people with type 2 diabetes

https://www.novonordisk.com/media/news-details.2226662.html

PIONEER 10:

Safety and Efficacy of Oral Semaglutide Versus Dulaglutide Both in Combination With One OAD (Oral Antidiabetic Drug) in Japanese Subjects With Type 2 Diabetes (PIONEER 10)

https://clinicaltrials.gov/ct2/show/NCT03015220

Oral semaglutide demonstrates greater reductions in HbA1c and body weight and comparable number of adverse events vs dulaglutide in Japanese people with type 2 diabetes

https://www.novonordisk.com/content/Denmark/HQ/www-novonordisk-com/en_gb/home/media/news-details.2216978.html

[/expand]

Novo Nordisk har acquired a priority review voucher for oral semaglutide for DKK800m, which will speed up the launch.

The long acting insulin 287 (LAI287) with a weekly injection has been promoted to phase 2 in the pipeline and LAIsema (LAI287 + semaglutide) is in phase 1. A few of the upcoming clinical trials on LAI287 include NCT03789578 (LAI287 with and without semaglutide in T2D cases) and NCT03751657 (comparison of weekly LAI287 with daily Insulin Glargine).

Press coverage

The earnings release triggered the following headlines and interviews.

Bloomberg: Novo Nordisk CEO Applauds Trump Plan to Limit Rebates

Reuters: Novo Nordisk’s new diabetes drug, outlook lift shares

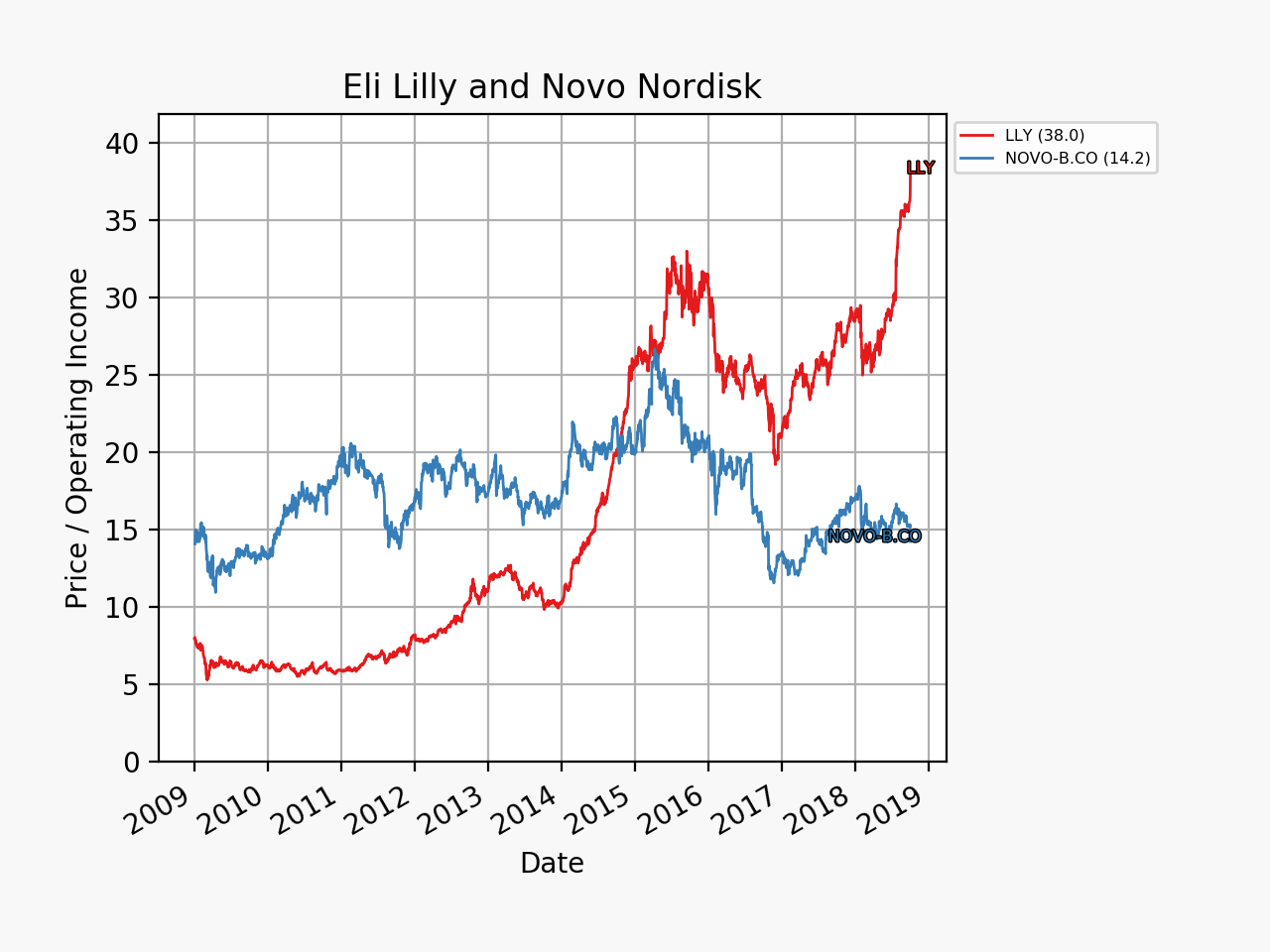

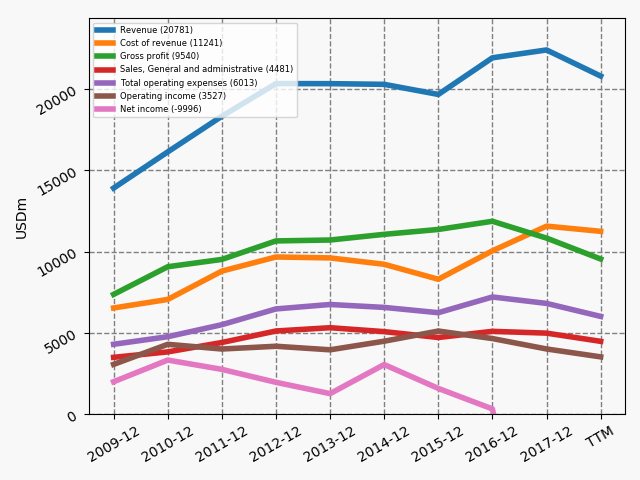

Financials

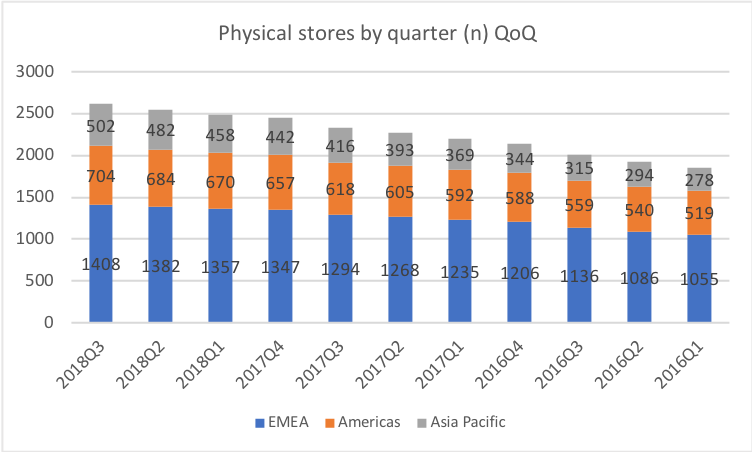

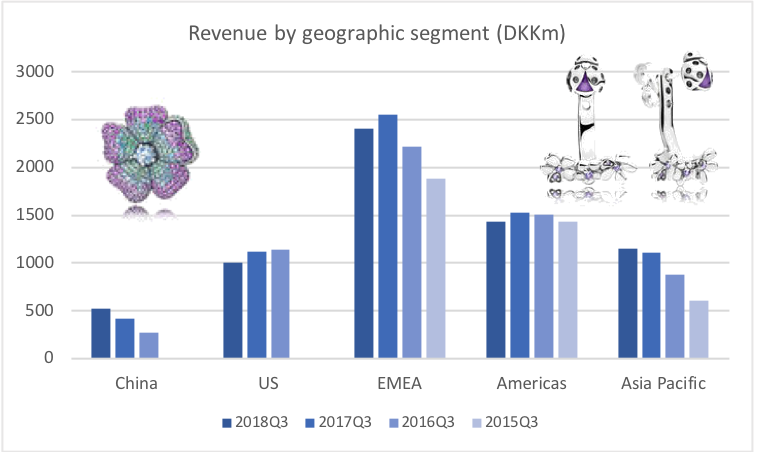

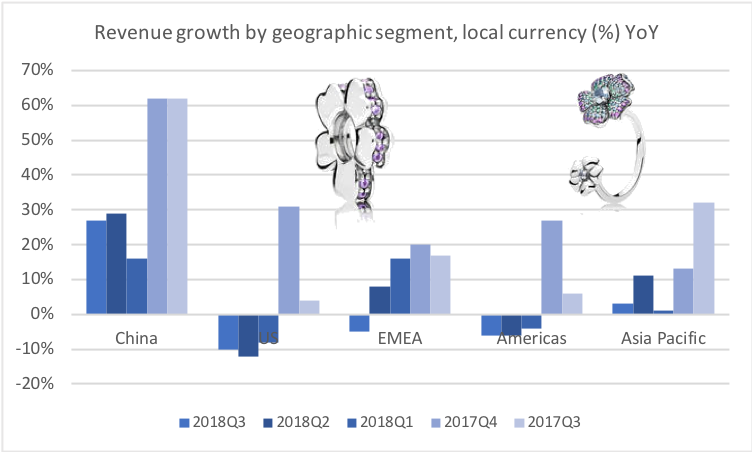

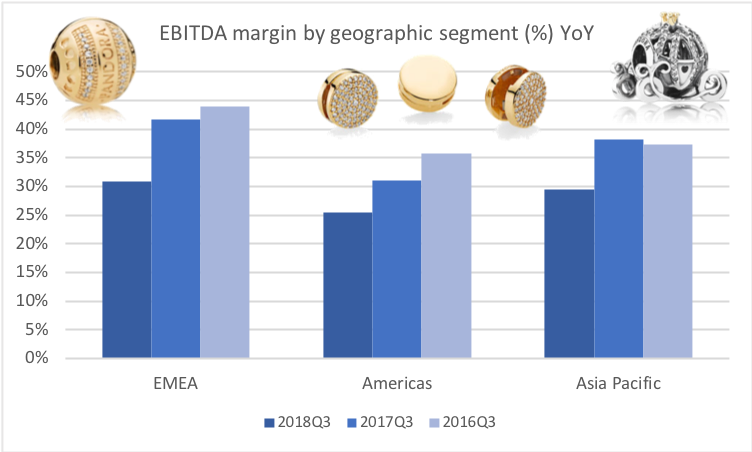

The figures below summarise some of the key financial metrics over the past 10 quarters and 10 years.

Future

The main event in 2019 for Novo Nordisk will probably be the launch of oral semaglutide. Here the expectation regarding approval from CSO Mads Krogsgaard Thomsen:

Novo Nordisk has notified the FDA that we will ask for a priority review for oral semaglutide based on the priority review voucher acquired in 2018. The use of the priority review voucher shortens the expected FDA review period to six months. We now expect to file the NDA for oral semaglutide with the FDA by the end of this quarter and in the EU and Japan in the second and third quarters of this year, respectively.

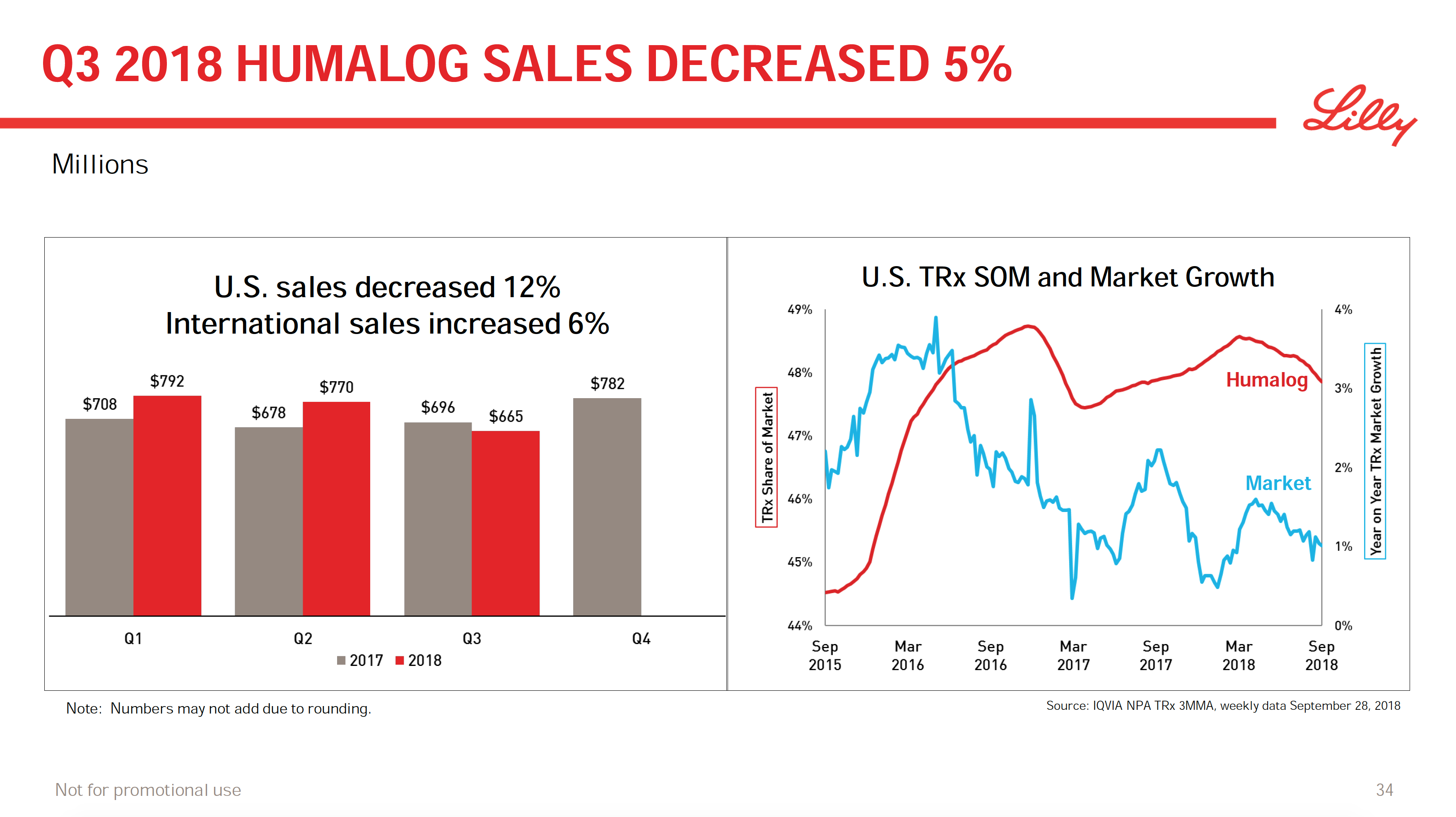

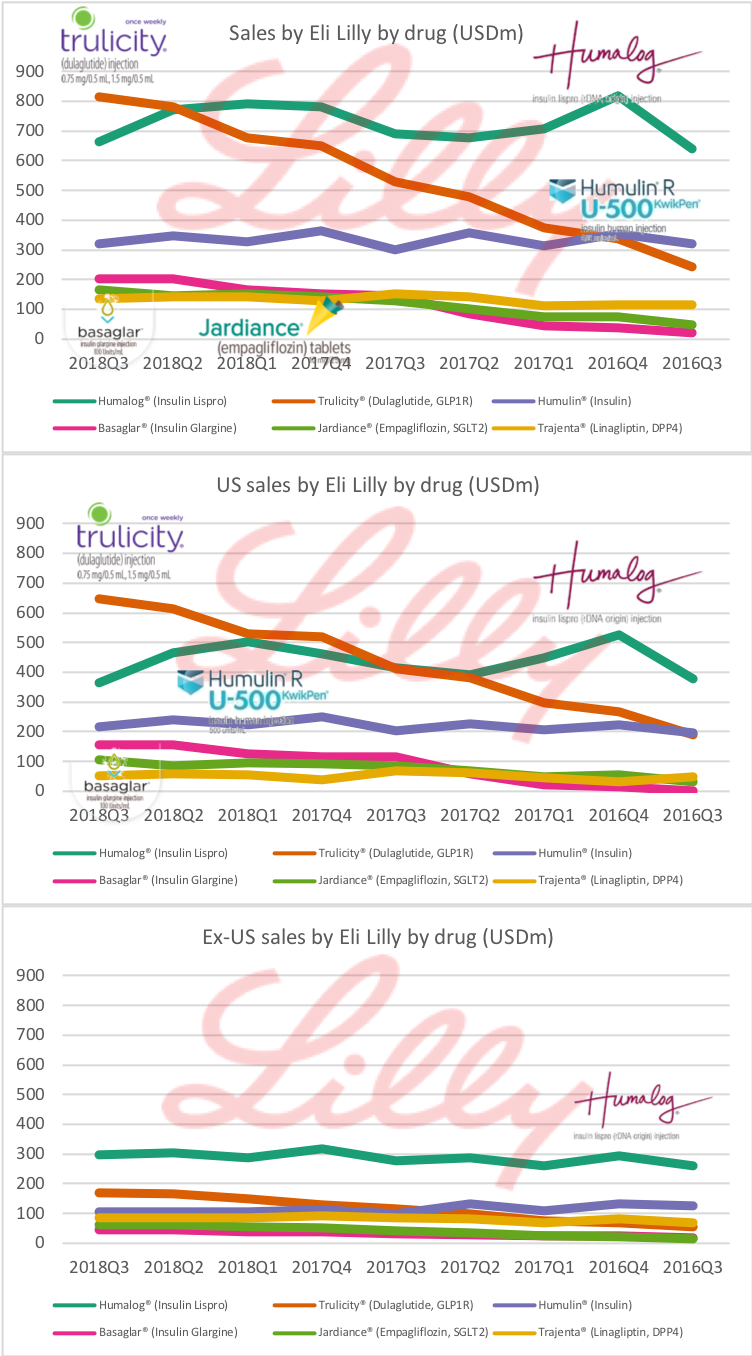

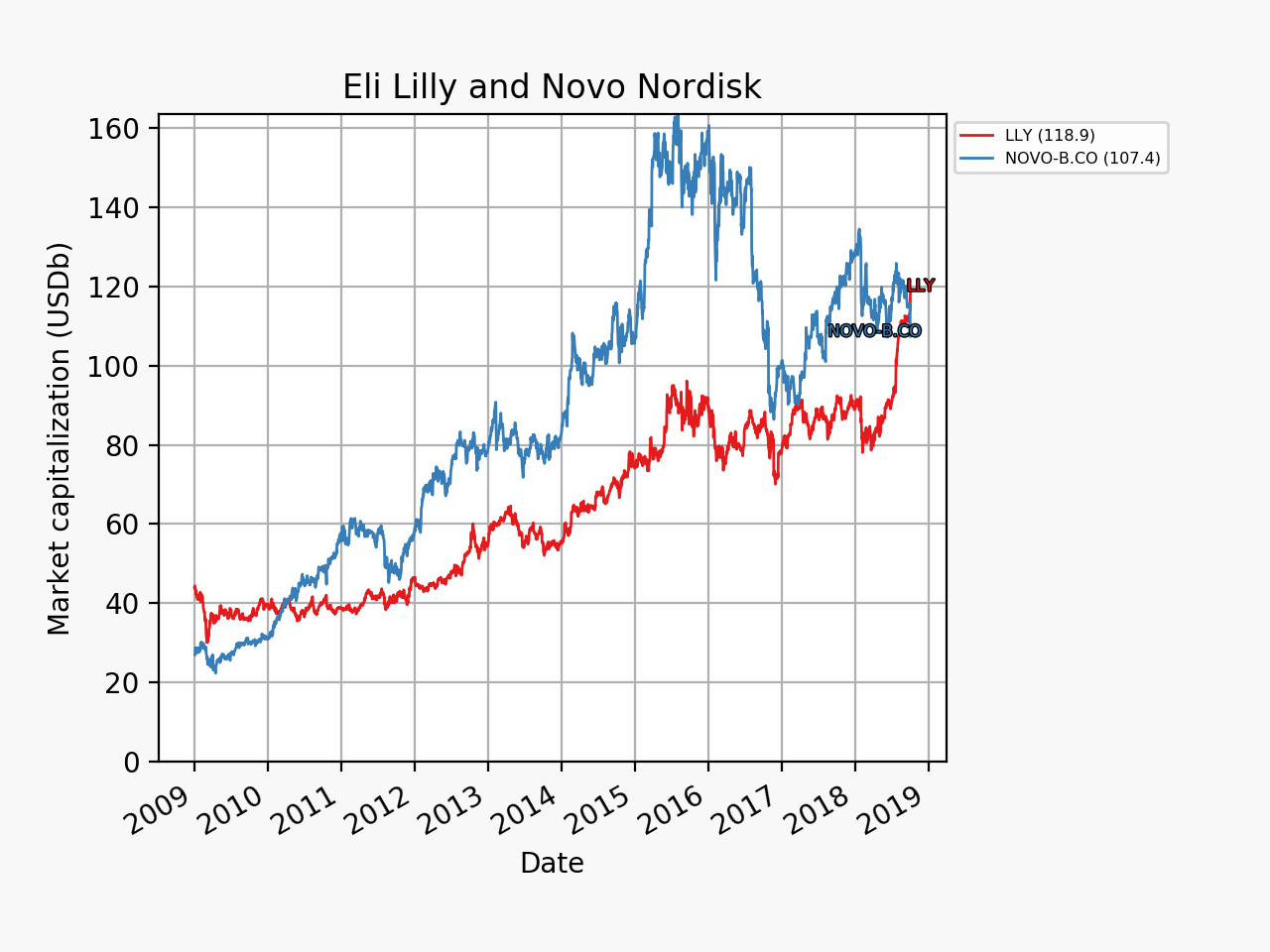

One would expect Ozempic® and Saxenda® to continue to contribute positively to the growth in 2019. The annual report from Eli Lilly will be released two weeks from now.